Credit Union Marketing Glossary: 100+ Terms Defined

Marketing terminology in the credit union space can be overwhelming — especially when your board asks about “GEO” and your VP wants to know the difference between CAC and CPL. This glossary cuts through the jargon.

We built this as a working reference for credit union marketing teams, executives, and board members who need to speak the same language as their agencies, vendors, and peers. Every term is defined in plain English with context for how it applies specifically to credit union marketing — not generic textbook definitions.

Bookmark this page. You’ll come back to it more than you think.

Key Takeaways

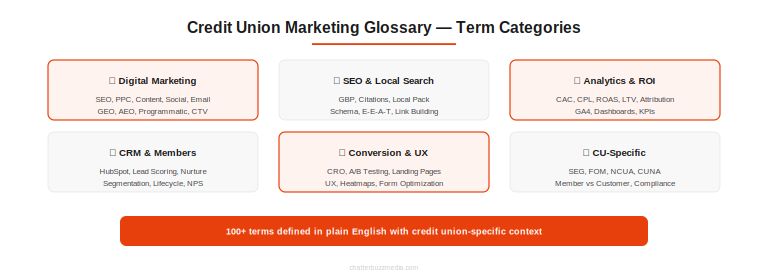

- This glossary covers 100+ marketing terms organized A-Z, each defined specifically for credit union context — not generic marketing definitions.

- Core categories include: digital marketing fundamentals, SEO and local search, paid media, content marketing, analytics and attribution, CRM and member engagement, and compliance.

- Use this as a team reference — share it with your board, marketing committee, and new hires to get everyone speaking the same language.

- Each term includes practical context: not just what it means, but why it matters for your credit union’s growth strategy.

Credit Union Marketing Glossary (A-Z)

A

ACH (Automated Clearing House)

An electronic network for financial transactions in the United States that processes large volumes of credit and debit transactions in batches. ACH transfers include direct deposit, payroll, consumer bills, tax refunds, and many other payment types.

Credit Union Context: ACH capabilities are fundamental to your digital banking infrastructure. Many members expect ACH functionality for bill pay, direct deposit, and person-to-person payments.

Why it Matters to a CU Marketer: When marketing digital banking services, highlighting seamless ACH capabilities can be a key differentiator. Understanding ACH also helps you market new products like instant payments or Zelle integration, which build upon traditional ACH infrastructure. Your messaging should emphasize convenience and security—both critical member concerns.

Advertising

The practice of promoting products, services, or brands through paid channels such as digital ads, print, broadcast, outdoor media, and sponsored content.

Credit Union Context: Unlike banks, credit unions operate as not-for-profit cooperatives, which means your advertising must emphasize member benefits, community focus, and competitive rates rather than shareholder profits.

Why it Matters to a CU Marketer: Your advertising strategy must comply with strict regulations (Truth in Savings, Truth in Lending) while differentiating your credit union’s member-first philosophy. Effective advertising drives awareness, but in the credit union world, it must also build trust and communicate your cooperative values. Track metrics like cost per lead and conversion rates to demonstrate ROI to leadership who may question marketing spend.

Affinity Marketing

A partnership between a company (credit union) and an organization that shares a customer base, allowing both to benefit from combined marketing efforts.

Credit Union Context: This strategy is deeply embedded in credit union DNA. Many credit unions were founded on affinity principles—serving employees of specific companies, members of associations, or residents of defined geographic areas. Your field of membership often defines natural affinity partnerships.

Why it Matters to a CU Marketer: Affinity marketing allows you to leverage existing trust relationships with employers, unions, associations, or community groups. These partnerships can dramatically reduce acquisition costs and improve conversion rates. Consider co-branded offerings, workplace financial education programs, or exclusive member benefits that reinforce both the affinity group and credit union brand.

Annual Percentage Rate (APR)

The yearly interest rate charged on borrowed money, including fees and other costs associated with the loan, expressed as a percentage.

Credit Union Context: Credit unions typically offer more competitive APRs than traditional banks due to their not-for-profit structure. This rate advantage is one of your strongest value propositions when marketing loans.

Why it Matters to a CU Marketer: APR is a critical element in all loan marketing communications and must be disclosed according to Truth in Lending Act (TILA) requirements. Your marketing materials must present APR clearly and conspicuously. When highlighting rate advantages, ensure your disclosures are compliant while still making the benefit clear to potential borrowers. Lower APRs directly support your acquisition goals for auto loans, personal loans, and mortgages.

Annual Percentage Yield (APY)

The effective annual rate of return on a deposit account, accounting for compound interest. APY shows members how much their savings will earn over a year.

Credit Union Context: Credit unions often offer competitive APYs on savings accounts, certificates, and money market accounts as a member benefit. This is a direct reflection of your not-for-profit status and member-focused mission.

Why it Matters to a CU Marketer: APY is your primary tool for marketing deposit products and must be displayed prominently in compliance with Truth in Savings Act regulations. When marketing deposit accounts, emphasize APY advantages over competitors to drive deposit growth—a key performance metric for your CFO. Remember that competitive APY also supports member retention by giving existing members reasons to consolidate their banking relationship with your institution.

Asset-Liability Management (ALM)

The practice of managing financial risks that arise from mismatches between assets (loans) and liabilities (deposits). ALM ensures that a credit union remains liquid and profitable while managing interest rate risk.

Credit Union Context: Your credit union’s ALM strategy directly impacts what rates you can offer on both the lending and deposit sides. It’s a fundamental consideration that shapes your entire product portfolio.

Why it Matters to a CU Marketer: Understanding ALM helps you grasp why your credit union may shift marketing emphasis between loans and deposits at different times. When your ALM team needs to grow deposits, your campaigns will focus on certificate specials and high-yield savings. When loan growth is the priority, you’ll emphasize competitive loan rates. This financial balancing act explains the strategic rationale behind your evolving marketing priorities and helps you communicate more effectively with your CFO.

Audience Segmentation

The process of dividing your target market into distinct groups based on shared characteristics such as demographics, behaviors, needs, or preferences, allowing for more personalized and effective marketing.

Credit Union Context: Effective segmentation in credit unions goes beyond basic demographics. Consider segmenting by life stage (first-time homebuyers, families, retirees), product usage (single-product vs. full-relationship members), digital engagement levels, and field of membership groups.

Why it Matters to a CU Marketer: Segmentation dramatically improves campaign performance and ROI. Rather than generic mass marketing, you can deliver targeted messages about relevant products—student loans to recent graduates, retirement planning to members approaching 55, or mobile banking features to digitally-engaged millennials. With limited marketing resources, segmentation ensures you focus your efforts where they’ll drive the highest returns. Proper segmentation also improves member experience by delivering relevant, timely communications rather than promotional noise.

B

Brand Equity

The commercial value derived from consumer perception of a brand name rather than the product or service itself. Strong brand equity means customers are willing to pay more, show greater loyalty, and advocate for your brand.

Credit Union Context: Credit unions often have strong brand equity within their field of membership communities, built on decades of trusted service, local reputation, and word-of-mouth. However, this equity may not extend beyond your core community.

Why it Matters to a CU Marketer: Building and protecting brand equity is essential for long-term growth and member retention. Your brand equity translates into lower acquisition costs (through referrals), higher lifetime value (through product adoption), and competitive insulation (members stay despite competitors’ rate offers). Measure brand equity through Net Promoter Score (NPS), member satisfaction surveys, and share of wallet metrics. Every marketing touchpoint either builds or erodes this equity—ensure consistency across channels.

Branch Transformation

The evolution of physical branch locations from traditional transaction centers to advisory and experience-focused environments, acknowledging that routine transactions have moved to digital channels.

Credit Union Context: While members increasingly handle transactions digitally, branches remain important for complex financial decisions, relationship building, and community presence. Branch transformation balances efficiency with maintaining your credit union’s personalized service reputation.

Why it Matters to a CU Marketer: Your marketing must evolve alongside branch transformation. Rather than promoting branch locations for basic transactions, emphasize advisory services, financial planning consultations, and community meeting spaces. Educate members on how to use digital channels for routine needs while positioning branches as trusted resources for significant financial decisions. This transformation also creates marketing opportunities around community events, financial education workshops, and localized campaigns.

BSA/AML (Bank Secrecy Act/Anti-Money Laundering)

Federal regulations requiring financial institutions to assist government agencies in detecting and preventing money laundering and terrorist financing activities.

Credit Union Context: Credit unions must maintain robust BSA/AML compliance programs, including customer identification programs, suspicious activity monitoring, and reporting requirements. These regulations significantly impact account opening processes and transaction monitoring.

Why it Matters to a CU Marketer: BSA/AML requirements affect member experience during account opening and may create friction that impacts conversion rates. Your marketing must set appropriate expectations about identification requirements and verification processes. When promoting new account offers or quick digital account opening, ensure your messaging aligns with the reality of compliance requirements. Understanding these constraints helps you develop realistic timelines and smoother onboarding experiences that balance compliance with member satisfaction.

C

CAC (Customer Acquisition Cost) / MAC (Member Acquisition Cost)

The total cost of acquiring a new customer or member, calculated by dividing all acquisition-related marketing and sales expenses by the number of new customers/members acquired in a specific period.

Credit Union Context: Member acquisition cost (MAC) is a critical metric for demonstrating marketing ROI to your board and executive team. In the credit union model, MAC should be calculated with a long-term perspective, as member relationships typically generate value over many years.

Why it Matters to a CU Marketer: Understanding your MAC by channel (digital ads, branch referrals, community events, direct mail) helps you optimize marketing spend. Compare MAC against member lifetime value (MLV) to ensure sustainable growth. If your MAC is $250 but the average member generates $1,000 in lifetime value, you can confidently invest in acquisition. Track MAC trends over time and benchmark against industry averages (typically $200-$400 for credit unions) to identify opportunities for improvement and efficiency.

Call-to-Action (CTA)

A specific instruction in marketing materials that prompts the audience to take a desired action, such as “Apply Now,” “Open an Account,” “Learn More,” or “Schedule an Appointment.”

Credit Union Context: Effective CTAs in credit union marketing must balance urgency with approachability. Your not-for-profit, member-first positioning means CTAs should feel helpful rather than overly aggressive or sales-focused.

Why it Matters to a CU Marketer: CTAs directly impact conversion rates across all channels—websites, emails, social media, ads, and branches. Test different CTA language, placement, and design to optimize performance. Strong CTAs clearly communicate the benefit (“Start Saving Today” vs. “Submit Form”) and create appropriate urgency without pressure. For complex products like mortgages, a softer CTA like “Speak with a Loan Officer” may outperform “Apply Now.” A/B test your CTAs continuously to improve campaign ROI.

Channels (Marketing)

The various platforms and methods used to reach and engage your target audience, including digital channels (website, email, social media, search engines) and traditional channels (branches, direct mail, print advertising, events).

Credit Union Context: Credit unions typically leverage an omnichannel approach, combining digital efficiency with personal, community-focused touchpoints. Your channel mix should reflect member preferences while maintaining your community-banking advantage.

Why it Matters to a CU Marketer: Different channels serve different purposes in the member journey. Digital channels excel at awareness and education; branches excel at trust-building and complex decisions. Understanding which channels drive the best results for specific goals (awareness vs. conversion) allows you to allocate limited marketing budget effectively. Track performance by channel to identify where to increase or decrease investment. Many credit unions over-invest in traditional channels due to comfort while under-investing in digital—review your channel mix quarterly against performance data.

CLV (Customer Lifetime Value) / MLV (Member Lifetime Value)

The total revenue a business expects to earn from a customer/member over the entire duration of their relationship, minus the costs of serving them.

Credit Union Context: Member lifetime value (MLV) in credit unions extends beyond simple profitability to include relationship depth (products per member), longevity, and referral value. A member who holds multiple products (checking, savings, auto loan, credit card, mortgage) and maintains the relationship for 15 years has significantly higher MLV than a single-product member.

Why it Matters to a CU Marketer: MLV justifies marketing investments and helps prioritize acquisition and retention strategies. If your average MLV is $1,200 but your best members generate $3,000+, you should invest more in acquiring similar profiles and deepening existing relationships. Use MLV to demonstrate marketing ROI: “Our $50,000 campaign investment acquired 200 members with projected lifetime value of $240,000.” Improve MLV through cross-selling, retention programs, and relationship deepening initiatives. Understanding MLV also guides decisions about when to invest in retaining at-risk members.

Compliance (Marketing)

Adherence to federal and state regulations governing financial services marketing, including Truth in Savings Act, Truth in Lending Act, Fair Lending laws, UDAAP regulations, and state-specific requirements.

Credit Union Context: Credit unions face the same marketing compliance requirements as banks but typically with smaller compliance teams and resources. Balancing compelling marketing with regulatory requirements is a constant challenge.

Why it Matters to a CU Marketer: Every marketing piece—from social media posts to billboard advertisements—must comply with complex regulations. Non-compliance risks regulatory action, fines, and reputation damage. Develop a marketing compliance review process that catches issues before materials go live. Common compliance pitfalls include missing APR/APY disclosures, misleading claims about rates or products, and inconsistent accessibility standards. Partner closely with your compliance team to ensure creativity doesn’t compromise regulatory adherence. Building strong compliance processes early prevents expensive mistakes later.

Content Marketing

A strategic marketing approach focused on creating and distributing valuable, relevant content to attract and engage a target audience, ultimately driving profitable customer action.

Credit Union Context: Content marketing aligns perfectly with credit unions’ educational mission and member-first philosophy. Your not-for-profit status gives you credibility to provide unbiased financial education that builds trust rather than pushing products.

Why it Matters to a CU Marketer: Quality content marketing drives organic search traffic, establishes thought leadership, and nurtures prospects through the consideration journey. Create content addressing common financial questions: “How to save for a down payment,” “Understanding credit scores,” “First-time homebuyer guide.” This content attracts prospects early in their journey, positions your credit union as a trusted resource, and keeps you top-of-mind when they’re ready to take action. Content marketing typically has lower acquisition costs than paid advertising and builds lasting brand equity. Learn more about developing an effective content marketing strategy for your credit union.

Conversion Rate Optimization (CRO)

The systematic process of increasing the percentage of website or app visitors who complete a desired action—such as submitting a loan application, opening an account, or scheduling an appointment.

Credit Union Context: Many credit union websites have strong traffic but poor conversion rates because they weren’t designed with conversion in mind. CRO focuses on removing friction from the member journey and making desired actions obvious and easy.

Why it Matters to a CU Marketer: Improving conversion rates multiplies the effectiveness of all your other marketing efforts. If you’re driving 10,000 monthly website visitors but only converting 1%, improving that to 2% doubles your results without increasing traffic costs. Focus on key conversion points: account applications, loan submissions, appointment requests, and email signups. Test elements like form length, CTA placement, trust signals, and page copy. Small improvements in conversion rates dramatically impact your member acquisition cost and overall marketing ROI. Explore our comprehensive conversion rate optimization services designed specifically for financial institutions.

Core System

The central banking platform that manages member accounts, transactions, deposits, loans, and reporting—essentially the operational backbone of your credit union.

Credit Union Context: Major core systems used by credit unions include Symitar, FIS, Corelation KeyStone, CUSO, and others. Your core system determines what’s technically possible for digital banking, data analytics, and marketing automation integration.

Why it Matters to a CU Marketer: Understanding your core system’s capabilities and limitations is essential for planning digital initiatives. Some cores offer robust APIs and modern integrations; others have significant technical constraints. Your core system determines how easily you can segment members for targeted campaigns, track product adoption, integrate marketing automation platforms, and implement personalized digital experiences. When evaluating new marketing technologies, always confirm compatibility with your core. Work closely with IT to understand what’s possible within your technical ecosystem.

CPA (Cost Per Acquisition)

A digital advertising metric that measures how much you spend to acquire one new customer, lead, or conversion through paid campaigns.

Credit Union Context: CPA varies significantly by product and channel. Member checking account acquisition might cost $50-$150, while mortgage application CPAs could range from $200-$500. Your credit union’s CPA benchmarks depend on your market, competition, and product mix.

Why it Matters to a CU Marketer: CPA is a fundamental metric for evaluating paid advertising campaign performance and ROI. Track CPA by channel (Google Ads, Facebook, display) and by product to identify your most efficient acquisition sources. Compare your CPA against member lifetime value to ensure profitable growth. If your checking account CPA is $100 but the member generates $800 in lifetime value, you have a sustainable model. Use CPA data to optimize campaigns, shifting budget toward high-performing channels and away from underperformers. Understanding digital marketing strategies for financial services can help you lower your CPA while improving results.

Credit Union (CU)

A member-owned, not-for-profit financial cooperative that provides traditional banking services to members who share a common bond (employer, association, or community). Credit unions operate on a one-member, one-vote principle rather than by shareholder ownership.

Credit Union Context: This foundational structure distinguishes you from banks and shapes everything you do. Your not-for-profit status means net income returns to members through better rates, lower fees, and improved services rather than shareholder dividends.

Why it Matters to a CU Marketer: Your credit union structure is your strongest differentiator but also one of the least understood by consumers. Many prospects don’t know what a credit union is or how membership works. Your marketing must educate prospects about the cooperative model while emphasizing tangible benefits: better rates, lower fees, personalized service, and community focus. Frame the credit union difference in terms prospects care about: “As a member, not a customer, you’re an owner. Your financial success is our only measure of success.” This positioning differentiates you from banks and online fintech competitors.

CRM (Customer Relationship Management) / MRM (Member Relationship Management)

Software systems that manage interactions with current and potential customers/members, tracking communication history, preferences, product ownership, and engagement across all touchpoints.

Credit Union Context: Many credit unions use “Member Relationship Management” (MRM) instead of CRM to reflect the member-focused language. Popular platforms for credit unions include HubSpot, Salesforce Financial Services Cloud, and industry-specific solutions like SugarCRM or Zoho.

Why it Matters to a CU Marketer: A robust CRM/MRM system is essential for effective marketing in today’s environment. It enables segmentation, personalization, automated workflows, lead scoring, and cross-selling opportunities. Without a proper CRM, you’re marketing blindly—unable to see who owns what products, who’s engaged vs. dormant, or who’s at risk of leaving. Modern CRM systems integrate with your core banking system, marketing automation platform, and communication channels to create a unified view of each member. This enables sophisticated lifecycle marketing that drives product adoption and deepens relationships. If you’re evaluating CRM platforms, explore our insights on marketing automation for financial institutions.

Cross-Selling

The practice of marketing additional products or services to existing customers/members based on their current relationship and needs.

Credit Union Context: Cross-selling is critical for credit unions because relationship depth drives profitability and loyalty. A member with only a savings account is far more likely to leave than one with checking, loans, credit card, and online banking. Your goal is to become your members’ primary financial institution.

Why it Matters to a CU Marketer: Cross-selling to existing members typically costs 5-10x less than acquiring new members while dramatically increasing lifetime value. Focus on logical product progressions: checking account holders need debit cards and mobile banking; auto loan customers are candidates for refinancing or vehicle insurance; young members who open savings accounts will eventually need checking, credit cards, and auto loans. Use data to identify cross-sell opportunities and time offers appropriately. Automated campaigns triggered by product ownership, life events, or behavioral signals (like checking balances that suggest savings capacity) drive efficient cross-selling at scale.

D

Debit Card / Credit Card

Payment cards that allow members to make purchases and access funds. Debit cards draw directly from checking accounts; credit cards provide revolving credit lines that must be repaid.

Credit Union Context: Card programs are significant revenue sources through interchange fees (debit) and interest income (credit), while also increasing member engagement. Many credit unions partner with networks like CO-OP or processors like PSCU for card services.

Why it Matters to a CU Marketer: Card adoption drives multiple benefits: increased member engagement (card usage creates frequent touchpoints), switching costs (members are less likely to leave if their card is connected to your account), and revenue. Market cards strategically: highlight debit cards to new checking account holders, credit cards to members seeking better rewards or rates than competitors. Emphasize benefits like fraud protection, mobile wallet integration, and rewards programs. Card activation campaigns shortly after account opening significantly improve engagement and retention.

Deposit Growth

The increase in total member deposits (savings, checking, certificates, money market accounts) over a specific period—a critical measure of credit union financial health.

Credit Union Context: Deposits fund your lending operations, so deposit growth directly enables loan growth and revenue generation. Your Asset-Liability Management (ALM) strategy balances deposit growth against lending goals to maintain healthy margins and liquidity.

Why it Matters to a CU Marketer: Deposit growth is typically one of your top strategic priorities and a key performance indicator for marketing effectiveness. Your CFO and board closely monitor deposit trends, especially given the competitive rate environment. Target deposit growth through competitive rate promotions on certificates and high-yield savings, campaigns emphasizing safety and NCUA insurance, and initiatives that increase account funding and usage. Track deposit acquisition cost similar to member acquisition cost to ensure efficient growth. When markets shift and deposits become expensive to acquire, pivot messaging toward relationship deepening and wallet share rather than new account acquisition.

Digital Branch

Online and mobile banking platforms that allow members to conduct most routine banking transactions without visiting a physical branch, including account management, transfers, deposits, bill pay, and loan applications.

Credit Union Context: Digital branch capabilities are no longer optional—they’re baseline expectations, especially for younger members. However, credit unions often lag behind banks and fintechs in digital experience, creating competitive vulnerabilities.

Why it Matters to a CU Marketer: Your digital branch is increasingly your primary member touchpoint, making it a critical marketing channel and conversion tool. Marketing must drive digital adoption among existing members (reducing operational costs) while showcasing digital capabilities to prospects (especially younger demographics). Emphasize convenience, security, and feature parity with competitors. Consider that many members still prefer human interaction for complex decisions—your marketing should position digital as convenient for routine needs while maintaining branch access for significant financial moments. Digital adoption rates are key metrics that directly impact operational efficiency and member satisfaction.

Digital Transformation

The comprehensive integration of digital technology into all areas of a credit union, fundamentally changing how you operate and deliver value to members, encompassing everything from online account opening to AI-powered chatbots.

Credit Union Context: Digital transformation in credit unions often lags behind traditional banks and fintech competitors due to legacy technology, limited resources, and cultural resistance to change. However, member expectations are forcing accelerated transformation.

Why it Matters to a CU Marketer: Digital transformation creates both challenges and opportunities for marketing. You must balance promoting new digital capabilities while managing member expectations about what’s possible. Your role includes driving adoption of new digital services through education and communication, gathering member feedback to inform product development, and positioning your credit union as modern and technologically capable despite resource constraints. Successful digital transformation requires marketing, IT, and operations to work closely together—ensure you’re involved in digital initiative planning from the beginning. Learn about leveraging AI in marketing to stay competitive during digital transformation.

Disclosures (Marketing)

Required legal language and information that must be included in financial marketing materials to comply with regulations like Truth in Savings, Truth in Lending, and state-specific requirements.

Credit Union Context: Disclosures can make financial marketing materials feel cluttered and legalistic, but they’re legally required. The challenge is incorporating required disclosures without undermining your marketing message or overwhelming the audience.

Why it Matters to a CU Marketer: Understanding disclosure requirements helps you design effective marketing materials from the start rather than treating compliance as an afterthought. Work with your compliance team to determine which disclosures are required for specific marketing pieces. Use design principles to make disclosures readable without dominating the message—appropriate font sizes, clear placement, and logical organization. For digital marketing (emails, social media, websites), ensure disclosures are appropriately accessible without requiring excessive scrolling or clicking. Disclosure management is a necessary skill for every financial services marketer.

Direct Marketing

Marketing communications sent directly to specific individuals or businesses through channels like direct mail, email, SMS, or targeted digital advertising, rather than mass media broadcasting.

Credit Union Context: Direct marketing allows credit unions to leverage their member data for targeted, personalized campaigns. You can reach specific member segments with relevant product offers based on demographics, product ownership, or behaviors.

Why it Matters to a CU Marketer: Direct marketing delivers higher response rates and ROI than broad awareness campaigns when executed with proper segmentation and personalization. Use direct mail for high-value products like mortgages or certificates (where higher costs are justified), email for regular communication and promotional offers (lower cost, faster deployment), and targeted digital advertising to reach specific demographics or behaviors. The key to direct marketing success is relevance—sending the right message to the right person at the right time. Poor direct marketing (irrelevant mass emails) damages your brand and member relationships.

E

Email Marketing

The practice of sending commercial or informational messages to a group of people via email, including newsletters, promotional campaigns, transactional emails, and automated nurture sequences.

Credit Union Context: Email marketing is one of your most cost-effective channels, providing direct access to members and prospects who’ve opted in to hear from you. Credit unions typically see higher open rates than many industries due to established trust relationships.

Why it Matters to a CU Marketer: Email marketing drives multiple strategic objectives: product promotion, member education, digital banking adoption, and relationship deepening. Build a comprehensive email strategy including monthly newsletters (brand awareness and education), promotional campaigns (product-specific offers), automated lifecycle emails (welcome series, product adoption, anniversary messages), and triggered behavioral emails (abandoned applications, low balance alerts, cross-sell opportunities). Segment your email lists for relevance and test subject lines, send times, and content to optimize performance. Track key metrics: open rates, click-through rates, conversion rates, and revenue per email. Avoid over-mailing, which leads to unsubscribes and disengagement.

Engagement (Member)

The level of interaction and involvement a member has with your credit union across all touchpoints, including digital banking usage, product ownership, branch visits, communication responsiveness, and relationship depth.

Credit Union Context: Engaged members are more profitable, loyal, and likely to recommend your credit union. Engagement indicators include login frequency, transaction volume, product diversity, and communication interactions. Disengaged members are retention risks.

Why it Matters to a CU Marketer: Member engagement is both a leading indicator of financial health (engaged members generate more revenue) and a key driver of long-term retention. Track engagement scores that combine digital activity, product ownership, and communication interactions to identify at-risk members who need intervention. Create engagement campaigns that encourage digital adoption, product trial, and regular interactions. Consider that engagement looks different for different members—a retiree might never use mobile banking but visit the branch monthly, while a millennial might bank entirely digitally. Define engagement appropriately for your member segments.

F

Fair Lending

Federal laws and regulations ensuring that all consumers have equal access to credit and are not discriminated against based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance.

Credit Union Context: Fair lending compliance affects every aspect of your lending operations and marketing. Credit unions must demonstrate fair treatment in marketing, underwriting, pricing, and servicing of all loan products.

Why it Matters to a CU Marketer: Marketing plays a critical role in fair lending compliance. Your campaigns must reach diverse communities, your messaging must not inadvertently discourage protected classes from applying, and your offers must be equally available to all qualified applicants. Avoid using language, images, or targeting that could be interpreted as discriminatory. When marketing in specific geographies or to specific groups, ensure you’re not neglecting protected classes or underserved communities. Partner with your compliance team to review campaigns for fair lending implications before launch. Fair lending violations carry severe penalties and reputation damage.

Field of Membership (FOM)

The defined group of people eligible to join a credit union, based on common bond requirements such as employment (SEG), association membership, family relationship, or geographic area.

Credit Union Context: Your field of membership determines your addressable market and shapes your entire business strategy. Some credit unions have narrow FOMs (single employer), while others have community charters covering entire regions.

Why it Matters to a CU Marketer: Understanding your FOM is fundamental to marketing strategy. It defines who you can legally serve, where to focus acquisition efforts, and how to position your brand. If your FOM is employer-based, workplace marketing and employee benefit positioning are critical. If you have a community charter, geographic targeting and local community involvement drive growth. When your FOM expands (adding SEGs or geographic areas), marketing must educate these new eligible populations about membership eligibility and benefits. Many credit unions under-leverage FOM expansion opportunities by failing to market proactively to newly eligible groups.

Financial Literacy Marketing

Marketing campaigns and content designed to educate members and prospects about personal finance topics such as budgeting, saving, investing, credit management, and homeownership.

Credit Union Context: Financial education aligns perfectly with credit unions’ cooperative mission and not-for-profit values. Unlike banks, you have no conflict of interest when providing unbiased financial guidance.

Why it Matters to a CU Marketer: Financial literacy content builds trust, establishes thought leadership, attracts prospects early in their financial journey, and positions your credit union as a valuable partner rather than just a transaction processor. Create educational content addressing common financial challenges: building emergency funds, improving credit scores, buying a first home, planning for retirement. This content drives organic search traffic, social media engagement, and community credibility. Consider offering workshops, webinars, one-on-one counseling, and online resources. Financial literacy marketing has longer ROI timelines than promotional campaigns but builds lasting brand equity and member loyalty.

FinTech (Financial Technology)

Technology-driven companies and innovations that compete with or complement traditional financial institutions, including digital-only banks, payment apps, robo-advisors, peer-to-peer lending platforms, and cryptocurrency services.

Credit Union Context: FinTech companies represent both threats and opportunities for credit unions. They often provide superior digital experiences and innovative products but lack credit unions’ community connections, personalized service, and full-service offerings.

Why it Matters to a CU Marketer: Understanding the FinTech competitive landscape helps you position your credit union effectively. Younger members especially are attracted to FinTech convenience and user experience, making them vulnerable to attrition if your digital capabilities lag. Your marketing must emphasize advantages that FinTech competitors can’t match: NCUA insurance, personalized human service, community commitment, and comprehensive financial solutions. Consider strategic FinTech partnerships that enhance your offering without requiring major technology investment. Position your credit union as combining the best of both worlds: FinTech convenience with traditional financial institution stability and service.

Fraud Prevention (Marketing for)

Communications designed to educate members about fraud risks and prevention strategies while promoting your credit union’s security features and fraud monitoring capabilities.

Credit Union Context: Credit unions are increasingly targets for fraud schemes, and members expect proactive protection. Fraud prevention marketing serves dual purposes: protecting members and demonstrating your commitment to their financial security.

Why it Matters to a CU Marketer: Fraud prevention marketing builds trust while reducing actual fraud losses that impact your bottom line. Educate members about common scams (phishing emails, fake calls, card skimming), promote security features (multi-factor authentication, transaction alerts, card controls), and communicate your fraud monitoring capabilities. Balance security messaging carefully—you want members to feel protected, not frightened. Regular fraud prevention communications also provide liability protection by demonstrating that you’ve educated members about security best practices. This content performs well on social media and email, driving strong engagement due to high relevance.

G

Geofencing

Location-based mobile advertising that targets people’s smartphones when they enter or exit defined geographic areas, such as competitor branches, retail locations, or specific neighborhoods.

Credit Union Context: Geofencing allows credit unions to reach prospects at highly relevant moments—when they’re near your branches or competitors’ locations. It’s particularly effective for local community credit unions with defined geographic footprints.

Why it Matters to a CU Marketer: Geofencing enables hyper-targeted acquisition campaigns with strong contextual relevance. Target competitor branches with messages about your better rates or service. Target retail areas with credit card offers or auto dealerships with loan promotions. Geofencing typically requires minimum investment but can deliver strong ROI when targeting is strategic and messaging is compelling. Track performance carefully—geofencing can waste budget if targeting is too broad or creative is irrelevant. Best results come from tight geographic parameters and offers that motivate immediate action. Learn more about geofencing advertising strategies for credit unions.

Google Analytics

A free web analytics platform that tracks and reports website traffic, user behavior, conversion paths, and campaign performance—the most widely used digital analytics tool.

Credit Union Context: Google Analytics provides essential insights about how members and prospects interact with your website: which pages they visit, how long they stay, where they drop off, and which marketing campaigns drive the most valuable traffic.

Why it Matters to a CU Marketer: Google Analytics is fundamental to data-driven marketing decision-making. Use it to understand which website pages perform well (and which need improvement), identify conversion bottlenecks in your digital applications, track campaign performance by traffic source, and demonstrate marketing ROI through goal completions and conversion tracking. Set up proper goal tracking for key actions: loan applications, account openings, appointment requests. Regularly review analytics data to inform content strategy, user experience improvements, and budget allocation. Without analytics, you’re marketing blindly—unable to optimize based on actual user behavior.

I

Indirect Lending

A loan origination model where loans are underwritten and funded through dealerships or other third-party partners rather than directly by the credit union, most common with auto loans.

Credit Union Context: Indirect lending allows credit unions to compete for auto loans at the point of sale—when members are at dealerships making purchase decisions. It dramatically expands your lending reach beyond members who proactively seek financing.

Why it Matters to a CU Marketer: Indirect lending programs require marketing to both consumers (building awareness that you offer competitive auto loans) and dealerships (establishing and maintaining dealer relationships). Support your indirect lending program through pre-approval campaigns that get members qualified before they shop, dealer relationship marketing that keeps you top-of-mind with F&I managers, and post-purchase communication that converts auto loan customers into full-relationship members. Indirect lending typically generates less profitable loans than direct lending but drives significant volume growth. Many indirect borrowers become long-term members if you effectively market additional products to them after their auto loan closes.

Influencer Marketing (Banking)

Partnering with individuals who have significant social media followings or community credibility to promote your credit union’s brand, products, or financial education content to their audiences.

Credit Union Context: While traditional celebrity influencers are rarely relevant for community credit unions, “micro-influencers” with local followings or niche credibility can be highly effective. Consider local business owners, community leaders, personal finance bloggers, or even satisfied members with social media presence.

Why it Matters to a CU Marketer: Influencer marketing provides authentic third-party credibility that traditional advertising can’t match, especially with younger demographics skeptical of corporate messaging. Partner with influencers who align with your values and genuinely support your mission. Influencer campaigns work well for financial literacy content, new product launches, and community initiatives. Ensure compliance review of influencer content and maintain FTC disclosure requirements. Micro-influencers with 10,000-100,000 followers often deliver better ROI than major influencers because their audiences are more engaged and their fees are more reasonable.

K

Keyword Research

The process of identifying search terms and phrases that potential members use when looking for financial services, products, or information online—fundamental to SEO and paid search strategies.

Credit Union Context: Keyword research for credit unions must balance broad financial terms (“auto loans,” “savings accounts”) with specific local and credit union-related terms (“credit union near me,” “join [CU name]”). Understanding search intent is critical—someone searching “credit union vs bank” is in a different stage than someone searching “apply for auto loan.”

Why it Matters to a CU Marketer: Keyword research informs multiple marketing initiatives: which content to create, how to structure website pages, what to bid on in paid search, and how to optimize for local SEO. Focus on high-intent keywords that indicate ready-to-buy mindsets (“mortgage pre-approval,” “open checking account”) rather than only informational terms. Consider long-tail keywords that are less competitive but highly relevant (“first-time homebuyer loans Orlando”). Local keywords are particularly valuable for community credit unions. Use keyword research tools like Google Keyword Planner, Semrush, or Ahrefs to identify opportunities and search volume. Revisit keyword strategy quarterly as search trends evolve.

KPI (Key Performance Indicator)

Quantifiable metrics that measure performance against strategic objectives, used to assess progress toward goals and inform decision-making.

Credit Union Context: Marketing KPIs for credit unions typically include member acquisition, deposit growth, loan volume, digital adoption rates, engagement metrics, cost per acquisition, return on advertising spend, and member satisfaction scores. Your KPIs should align directly with institutional strategic priorities.

Why it Matters to a CU Marketer: KPIs provide objective evidence of marketing effectiveness and justify marketing investments to leadership. Define clear KPIs for every campaign and initiative, tracking both activity metrics (website traffic, email open rates) and outcome metrics (applications submitted, accounts opened, loans funded). Dashboard your KPIs for regular review and trend analysis. When presenting to leadership, focus on outcome KPIs that directly tie to business objectives rather than vanity metrics. For example, “We generated 150 new member accounts” matters more than “Our Facebook page gained 500 followers.” Strong KPI tracking demonstrates marketing’s business impact and guides budget allocation toward highest-performing initiatives.

L

Landing Page

A standalone web page created specifically for a marketing campaign, designed to convert visitors by focusing on a single call-to-action without navigation distractions.

Credit Union Context: Landing pages are essential for campaign effectiveness, providing focused experiences that align with specific ads or promotions. A landing page for a certificate special should focus exclusively on that offer, not on your full product menu.

Why it Matters to a CU Marketer: Landing pages typically convert 2-5x better than sending traffic to generic website pages because they eliminate distractions and maintain message consistency from ad to page. Create dedicated landing pages for significant campaigns: new member promotions, limited-time rate offers, mortgage campaigns, and digital banking adoption. Essential landing page elements include clear headline matching your ad, compelling benefits, trust signals (NCUA insurance, awards), simple form, and strong call-to-action. Test variations to optimize conversion rates. Track landing page performance separately for each campaign to identify what works and replicate success. Learn the crucial components every landing page needs to convert leads effectively.

Lead Generation

The process of attracting and capturing interest from potential members who haven’t yet joined your credit union but have expressed interest through actions like completing a contact form, downloading content, or requesting information.

Credit Union Context: Lead generation for credit unions happens across multiple channels: website forms, community events, branch walk-ins, referrals, and digital campaigns. Effective lead generation requires both capturing contact information and having systems to nurture leads toward membership.

Why it Matters to a CU Marketer: Lead generation feeds your membership growth engine. Many prospects need multiple touchpoints before joining, so capturing leads early allows you to nurture them through the decision journey. Implement lead capture mechanisms on your website (chatbots, forms, content downloads), at events (digital sign-up tablets), and through advertising (lead-generation campaigns). Develop lead nurturing workflows that provide value, build trust, and gradually move prospects toward membership. Track lead conversion rates to identify where prospects drop off and optimize your process. Compare the ROI of different lead generation channels to focus investment on your most effective sources. Discover proven B2B lead generation strategies that work for financial institutions.

Loan Volume

The total dollar amount of loans originated during a specific period—a critical revenue driver and strategic priority for most credit unions.

Credit Union Context: Loan volume directly impacts your credit union’s income, as interest on loans is typically your largest revenue source. Loan volume goals are usually broken down by product type (mortgage, auto, personal, business) and tracked monthly and annually.

Why it Matters to a CU Marketer: Driving loan volume is typically one of your primary marketing objectives. Marketing strategies that support loan growth include competitive rate promotions, pre-approval campaigns, seasonal campaigns (auto loans in spring, home equity before summer, mortgages in peak home-buying season), referral incentives, and cross-selling to existing members. Track which marketing channels and campaigns drive the most valuable loan applications—not just volume, but quality applications that convert to funded loans. Work closely with lending teams to understand capacity constraints, rate competitiveness, and approval criteria so your marketing targets realistic opportunities. Demonstrate marketing ROI by tracking loan volume generated from specific campaigns against the cost of those campaigns.

Local SEO

Search engine optimization tactics focused on improving visibility in local search results and Google Maps, particularly important for businesses with physical locations like credit union branches.

Credit Union Context: Local SEO is critical for credit unions because most searches for financial services include local intent (“credit union near me,” “auto loans in Orlando”). Strong local SEO ensures your branches appear in “near me” searches and Google Maps results.

Why it Matters to a CU Marketer: Local SEO drives high-intent traffic from prospects actively searching for your services in your community. Optimize for local SEO through accurate Google Business Profile listings for every branch, consistent NAP (name, address, phone) information across all online directories, location-specific website pages with unique content, local keywords in page titles and content, member reviews on Google and other platforms, and local link building from community organizations. Local SEO delivers sustained organic visibility without ongoing ad spend, making it highly cost-effective long-term. Track rankings for priority local keywords and your Google Business Profile performance metrics. For community credit unions, local SEO should be a top digital marketing priority. Discover how to optimize your Google Business Profile for maximum local visibility.

M

Marketing Automation

Software platforms that automate repetitive marketing tasks such as email campaigns, social media posting, lead nurturing, and customer segmentation based on triggers, behaviors, and predefined workflows.

Credit Union Context: Marketing automation allows small marketing teams to execute sophisticated, personalized campaigns at scale. Popular platforms for credit unions include HubSpot, Salesforce Marketing Cloud, ActiveCampaign, and credit union-specific solutions integrated with core systems.

Why it Matters to a CU Marketer: Marketing automation multiplies your team’s effectiveness, enabling you to deliver timely, relevant communications without manual effort. Implement automated workflows for new member onboarding, product cross-selling based on account activity, re-engagement of dormant members, loan application follow-up, abandoned application recovery, and lifecycle campaigns tied to member tenure or life events. Automation ensures no prospect or member falls through the cracks while delivering consistent, personalized experiences. Start with simple automations (welcome series, birthday messages) and expand to more sophisticated behavioral triggers as your proficiency grows. Marketing automation typically delivers 5-10x ROI for credit unions that implement it effectively. Explore our comprehensive guide to marketing automation for financial services.

Member Experience (MX)

The comprehensive perception and feeling members have about all their interactions with your credit union across every touchpoint—branches, website, mobile app, phone support, and communications.

Credit Union Context: Member experience is increasingly recognized as a key competitive differentiator. While credit unions traditionally compete on rates and service, exceptional member experience creates emotional loyalty that transcends rate shopping and drives referrals.

Why it Matters to a CU Marketer: Marketing’s role extends beyond acquisition to encompass the entire member journey. You’re responsible for setting expectations through your messaging, ensuring brand promise alignment with actual experience, designing seamless digital experiences, and communicating in ways that feel personalized and relevant. Poor member experience undermines marketing effectiveness—if your ads promise “easy digital banking” but your mobile app is clunky, you create dissatisfaction and churn. Map member journeys to identify pain points and opportunities for improvement. Collect and analyze member feedback to inform experience enhancements. Partner with operations to ensure marketing promises match reality. In today’s competitive environment, exceptional member experience is your sustainable competitive advantage.

Member Relationship Management (MRM)

Credit union-specific terminology for Customer Relationship Management (CRM) systems, emphasizing the member-owner relationship rather than transactional customer relationship.

Credit Union Context: The term “Member Relationship Management” reflects credit unions’ philosophical distinction between members (owners) and customers (transactional relationships). While functionally similar to CRM, the terminology emphasizes partnership over transaction.

Why it Matters to a CU Marketer: Using MRM language reinforces your credit union’s cooperative identity and member-first philosophy in internal communications and member-facing materials. An MRM system enables you to manage and deepen member relationships through comprehensive data about product ownership, interaction history, preferences, and behaviors. This data powers personalized marketing, identifies cross-sell opportunities, flags at-risk members, and supports relationship-based service delivery. Whether you call it CRM or MRM, the capability is essential for effective modern marketing. Implement an MRM system that integrates with your core to create a unified member view that informs every marketing decision and campaign.

Mobile Banking

Financial services and account management delivered through smartphone or tablet applications, including balance checking, transfers, mobile deposits, bill pay, and card management.

Credit Union Context: Mobile banking has evolved from a nice-to-have feature to a baseline member expectation, especially for younger demographics. Credit unions that fail to offer competitive mobile banking experiences face significant member satisfaction and retention challenges.

Why it Matters to a CU Marketer: Mobile banking adoption drives multiple benefits: increased engagement, reduced operational costs (fewer branch transactions), higher member satisfaction, and improved retention. Marketing must drive mobile app downloads and active usage among existing members while showcasing mobile capabilities to prospects. Create campaigns encouraging mobile enrollment, educate members on features they’re not using, highlight convenience and security benefits, and showcase updates when new features launch. Track mobile banking adoption rates by member segment and develop targeted campaigns for laggards. For younger prospects, mobile banking capabilities often determine whether they’ll consider your credit union at all—ensure your marketing accurately represents your mobile experience quality.

N

NCUA (National Credit Union Administration)

The independent federal agency that charters and supervises federal credit unions and insures deposits at all federal credit unions and most state-chartered credit unions through the National Credit Union Share Insurance Fund.

Credit Union Context: NCUA is to credit unions what the FDIC is to banks—the regulatory body and deposit insurer. NCUA insurance protects member deposits up to $250,000, providing the same safety as FDIC insurance at banks.

Why it Matters to a CU Marketer: NCUA insurance is a critical trust factor that should be prominently featured in your marketing. Many consumers don’t understand that credit union deposits are federally insured with the same protection as bank deposits, creating potential concerns about safety. Display the NCUA insurance logo prominently on your website, marketing materials, and branches. In competitive situations against banks, emphasize that your deposits are “Federally insured to at least $250,000 and backed by the full faith and credit of the United States Government” to overcome any safety concerns. NCUA also issues regulations affecting marketing compliance—stay current on regulatory guidance relevant to advertising and member communications.

NPS (Net Promoter Score)

A customer loyalty metric that measures how likely members are to recommend your credit union to others, calculated by asking “On a scale of 0-10, how likely are you to recommend us to a friend or colleague?”

Credit Union Context: Credit unions typically score higher on NPS than traditional banks due to member-focused service and cooperative structure. Strong NPS indicates member satisfaction and predicts growth through referrals—one of credit unions’ most cost-effective acquisition channels.

Why it Matters to a CU Marketer: NPS provides a simple, trackable metric of member satisfaction and loyalty. Survey members regularly to measure NPS, identify detractors who need intervention, and cultivate promoters as referral sources. Investigate the drivers behind your NPS—what creates promoters vs. detractors? Address root causes of detractor experiences while amplifying what creates promoters. Use NPS success in marketing materials: “95% of our members would recommend us to friends and family.” Strong NPS also justifies investment in member experience initiatives by demonstrating the business value of satisfaction. Track NPS trends over time and by member segment to ensure your marketing and service strategies are building loyalty.

O

Online Banking

Web-based banking platforms that allow members to manage accounts, view transactions, transfer funds, pay bills, and conduct other banking activities through internet browsers on computers or mobile devices.

Credit Union Context: Online banking is now table stakes for credit unions, with members expecting 24/7 account access and full transaction capabilities. While distinct from mobile banking (app-based), online banking remains critical for members who prefer desktop/laptop access.

Why it Matters to a CU Marketer: Online banking adoption is essential for operational efficiency and member satisfaction. Marketing should drive enrollment among members still conducting business exclusively in branches or by phone, emphasizing convenience, security, 24/7 access, and features like e-statements and mobile deposits. Create educational campaigns that reduce adoption barriers (security concerns, technical complexity) through simple how-to content and support resources. Track online banking adoption rates and target non-adopters with enrollment campaigns. For prospects, showcase your online banking capabilities during the consideration phase to demonstrate that your credit union offers the digital convenience they expect.

Omnichannel Marketing

An integrated marketing approach that provides seamless, consistent member experiences across all channels and touchpoints—digital, branch, phone, email, mobile—with coordinated messaging and data sharing.

Credit Union Context: Omnichannel marketing means a member might start a loan application on mobile, continue on desktop, visit a branch for questions, and complete it online—with each touchpoint informed by the previous interactions. True omnichannel requires integration between your core system, CRM, website, marketing automation, and branch systems.

Why it Matters to a CU Marketer: Members expect seamless experiences across channels, not disconnected interactions that require them to repeat information. Implement omnichannel marketing to improve conversion rates (by removing friction across channels), increase satisfaction (through personalized, informed interactions), and maximize marketing ROI (by coordinating rather than duplicating efforts across channels). Start by ensuring consistent branding and messaging across all channels, then work toward data integration that creates unified member views, and ultimately develop coordinated campaigns that guide members through optimal channel journeys. Omnichannel marketing is complex but delivers significantly better results than channel-siloed approaches.

Open Banking

A banking practice that provides third-party financial service providers access to consumer banking data through APIs (application programming interfaces), enabling innovative financial services and products.

Credit Union Context: Open banking is still emerging in the U.S. credit union sector but is becoming increasingly important as members use financial management tools, payment apps, and robo-advisors that require account connectivity.

Why it Matters to a CU Marketer: Open banking creates both opportunities and threats. On the opportunity side, it enables you to offer enhanced services through fintech partnerships—budgeting tools, aggregated financial views, and innovative payment options. On the threat side, it allows competitors to access your members’ data to market competing products. Marketing should educate members about open banking benefits while emphasizing security and control over data sharing. Position your credit union as forward-thinking by supporting useful integrations while maintaining strong data privacy and security. As open banking evolves, ensure your marketing messaging stays current with member concerns and competitive positioning.

P

PPC (Pay-Per-Click)

A digital advertising model where advertisers pay each time someone clicks on their ad, most commonly associated with search engine advertising (Google Ads) and social media advertising (Facebook, LinkedIn).

Credit Union Context: PPC is one of the most effective channels for credit unions to drive qualified traffic and leads because it captures prospects actively searching for financial services. PPC requires ongoing management and optimization to maintain cost-effectiveness.

Why it Matters to a CU Marketer: PPC delivers measurable, scalable results for priority products and campaigns. Use PPC for high-intent keywords (“auto loan rates,” “join credit union”), geographic targeting to reach your field of membership, competitor targeting to capture rate shoppers, and retargeting to re-engage website visitors who didn’t convert. Track key metrics: click-through rate (CTR), conversion rate, cost per click (CPC), cost per acquisition (CPA), and return on ad spend (ROAS). PPC requires continuous optimization—pause underperforming keywords, refine targeting, test ad copy, and improve landing pages. Many credit unions waste PPC budget on poorly targeted campaigns or generic landing pages—invest in proper management to ensure positive ROI. Learn about Google Ads best practices specific to financial services.

Product/Service Lifecycle (Credit Union)

The stages a financial product moves through from introduction to maturity to eventual decline, requiring different marketing strategies at each stage: launch (awareness), growth (adoption), maturity (optimization), and decline (phase-out or refresh).

Credit Union Context: Credit unions must manage product lifecycles for various offerings—checking accounts, loan products, certificate terms, and credit cards. Product lifecycle management ensures your portfolio stays competitive and relevant to member needs.

Why it Matters to a CU Marketer: Different lifecycle stages require different marketing approaches. New product launches need broad awareness campaigns and member education. Growth-stage products need targeted acquisition and adoption campaigns. Mature products need optimization and competitive positioning. Declining products need strategic phase-out or reinvention. Understanding product lifecycle helps you allocate marketing resources appropriately—heavy investment in promising growth products, maintenance spending on mature products, and strategic decisions about declining products. Work with product management to understand lifecycle status of your portfolio and align marketing strategy accordingly.

R

Remarketing/Retargeting

Digital advertising that targets people who have previously interacted with your brand—visited your website, watched a video, or engaged with social media—by showing them relevant ads as they browse other sites or platforms.

Credit Union Context: Remarketing allows credit unions to stay top-of-mind with prospects who showed interest but didn’t convert initially. This is particularly valuable for high-consideration products like mortgages or auto loans where decision timelines extend over weeks or months.

Why it Matters to a CU Marketer: Remarketing typically delivers strong ROI because you’re targeting warm audiences that already know your brand. Implement remarketing to re-engage website visitors who didn’t complete applications, target specific product page visitors with relevant offers, promote limited-time offers to previous visitors, and maintain awareness with prospects during extended decision journeys. Segment your remarketing audiences by behavior—someone who visited mortgage pages should see mortgage ads, not generic credit union messages. Set frequency caps to avoid ad fatigue and negative brand perception. Remarketing fills a critical gap in the marketing funnel by nurturing prospects who aren’t yet ready to convert but shouldn’t be abandoned.

ROI (Return on Investment)

A performance metric that measures the profit or value generated by an investment relative to its cost, calculated as (Revenue – Cost) / Cost, typically expressed as a percentage or ratio.

Credit Union Context: Marketing ROI for credit unions must account for member lifetime value rather than just immediate revenue. A $50,000 campaign that acquires 100 members with average lifetime value of $1,200 generates $120,000 in value—a 140% ROI even though revenue isn’t immediate.

Why it Matters to a CU Marketer: Demonstrating marketing ROI is essential for securing budget and leadership support, especially when competing for resources with operations and technology initiatives. Calculate ROI for significant campaigns and initiatives, tracking both direct revenue impact (loan volume, deposit growth) and longer-term value (member acquisition, retention improvements). Present ROI data regularly to leadership, showing how marketing investments drive business outcomes. When ROI is negative or unclear, diagnose why and adjust strategy. Strong ROI documentation transforms marketing from a cost center to a recognized growth driver. Include member lifetime value in ROI calculations to accurately reflect long-term marketing impact.

ROAS (Return on Ad Spend)

A marketing metric that measures revenue generated per dollar spent on advertising, calculated as Revenue / Ad Spend. ROAS of 3:1 means every dollar spent generates three dollars in revenue.

Credit Union Context: ROAS is most relevant for direct-response advertising campaigns with clear conversion tracking—digital ads for specific loan products or deposit accounts where you can track applications and funding through to revenue.

Why it Matters to a CU Marketer: ROAS provides clear accountability for advertising effectiveness and guides budget allocation across channels and campaigns. Track ROAS for paid search, paid social, display advertising, and other direct-response channels. Compare ROAS across products to identify your most efficient advertising opportunities—if mortgage ads generate 5:1 ROAS while personal loan ads generate 2:1, shift budget accordingly. Improve ROAS through better targeting, more compelling creative, optimized landing pages, and improved conversion processes. Note that ROAS is less relevant for brand awareness campaigns that don’t drive immediate conversions—use appropriate metrics for different campaign objectives.

Responsive Design

A web design approach that ensures websites adapt seamlessly to different screen sizes and devices—desktops, tablets, and smartphones—providing optimal viewing and interaction experiences across all platforms.

Credit Union Context: With over 60% of website traffic now coming from mobile devices, responsive design is non-negotiable for credit unions. Members expect seamless experiences regardless of how they access your site.

Why it Matters to a CU Marketer: Responsive design directly impacts conversion rates, user experience, search engine rankings, and brand perception. Google prioritizes mobile-friendly sites in search results, so responsive design affects your SEO performance. Poor mobile experiences drive high bounce rates and lost conversions—if your loan application process doesn’t work smoothly on mobile, you’re losing applicants. Ensure your website, landing pages, email templates, and all digital properties use responsive design. Test across multiple devices and screen sizes regularly. Responsive design is a foundational requirement for effective digital marketing—get this right or all your traffic-driving efforts will be undermined by poor user experience.

Retention Marketing

Marketing strategies and campaigns focused on keeping existing members engaged, satisfied, and loyal rather than acquiring new members, including loyalty programs, engagement campaigns, and win-back initiatives.

Credit Union Context: Retention is typically more cost-effective than acquisition (5-10x less expensive) and directly impacts profitability since long-term members generate significantly more lifetime value. Credit unions generally have strong retention due to relationship banking models but still face attrition risks.

Why it Matters to a CU Marketer: Retention marketing deserves substantial focus alongside acquisition efforts. Implement retention strategies including regular communication that maintains engagement, product cross-selling that deepens relationships, proactive service outreach at key moments, milestone recognition (account anniversaries, loan payoffs), win-back campaigns for dormant members, and loyalty programs that reward tenure and engagement. Identify at-risk members through behavior monitoring (declining engagement, competitive shopping, single-product relationships) and intervene proactively. Calculate retention rates by member segment and track improvement from retention initiatives. Even small improvements in retention rate dramatically impact long-term growth and profitability.

S

SEG (Select Employer Group)

A company or organization whose employees are eligible for credit union membership, typically through a formal partnership or affiliation that becomes part of the credit union’s field of membership.

Credit Union Context: SEG expansion is a primary growth strategy for many credit unions, allowing you to add new eligible populations without changing your charter type. Building relationships with employers and associations creates natural pathways for member acquisition.

Why it Matters to a CU Marketer: SEG marketing requires a two-pronged approach: partnering with organizations to establish SEG relationships, then marketing to employees/members of those organizations to drive actual membership. Develop marketing collateral for SEG prospecting that emphasizes benefits to both the organization and its people. Once a SEG is established, leverage workplace marketing tactics: employee benefit fairs, payroll promotions, direct payroll deposit campaigns, financial wellness programs, and exclusive offers for SEG members. Track SEG performance individually to identify your most valuable relationships and replicate successful models. SEG partnerships provide warm audiences with implicit endorsements, typically delivering lower acquisition costs than broad geographic marketing.

SEO (Search Engine Optimization)

The practice of optimizing websites and content to rank higher in organic (non-paid) search engine results, driving qualified traffic through improved visibility for relevant search queries.

Credit Union Context: SEO is critical for credit unions because most financial services searches start with Google. Strong organic rankings for priority keywords (“credit union [city],” “auto loan rates [city],” “mortgage lenders near me”) drive sustained, cost-effective traffic.

Why it Matters to a CU Marketer: SEO delivers compounding long-term value—unlike paid advertising that stops when you stop spending, SEO improvements continue generating traffic indefinitely. Focus on local SEO (ranking for geographic searches), content SEO (creating pages targeting specific keywords), and technical SEO (site speed, mobile optimization, structured data). Develop content addressing common financial questions and services to capture informational and transactional searches. Build quality backlinks from local organizations, community sites, and industry directories. Track rankings for priority keywords and organic traffic trends. SEO requires patience—results typically take 3-6 months to materialize—but delivers exceptional long-term ROI. Partner with experienced SEO services that understand credit union marketing.

SERP (Search Engine Results Page)

The page displayed by search engines in response to a user’s query, showing a combination of organic results, paid ads, featured snippets, local results, and other search features.

Credit Union Context: Understanding SERP layout helps you optimize for maximum visibility. For local credit union searches, the SERP typically includes a local map pack (top 3 Google Business Profile listings), followed by organic results and paid ads.

Why it Matters to a CU Marketer: SERP position dramatically affects click-through rates—the #1 organic result receives roughly 30% of clicks, #2 receives 15%, and rankings beyond page 1 receive minimal traffic. Optimize to appear in SERP features like featured snippets (answer boxes), local pack listings, and “People Also Ask” sections for increased visibility. Monitor SERPs for priority keywords to understand what appears and how to improve your presence. SERP analysis also reveals competitive intelligence about what content and messaging competitors emphasize. Changes to SERP layouts (more ads, fewer organic results) may require strategy adjustments to maintain visibility.

Share of Wallet (SOW)

The percentage of a member’s total financial services spending that goes to your credit union versus competitors, measuring relationship depth and market penetration.

Credit Union Context: Share of wallet is a critical metric for credit unions because members who consolidate their financial relationships with you are more profitable, loyal, and valuable. A member using you only for savings but getting loans elsewhere represents a share of wallet opportunity.

Why it Matters to a CU Marketer: Increasing share of wallet through cross-selling and relationship deepening is typically more profitable than new member acquisition. Measure share of wallet by tracking products per member and comparing to external benchmark data about typical household product ownership. Target members with low share of wallet for cross-sell campaigns—if someone has only savings, they likely need checking; if they have only deposits, they likely need loans. Position your credit union as a “primary financial institution” rather than just another account. Survey members about which products they use elsewhere and why, addressing barriers to consolidation. Even small improvements in share of wallet multiply the value of your existing member base.

Social Media Marketing

Marketing activities conducted on social media platforms like Facebook, Instagram, LinkedIn, TikTok, and others to build brand awareness, engage members, drive website traffic, and generate leads.