The financial services landscape is undergoing seismic shifts. Credit unions that once relied on branch traffic and traditional community outreach now find themselves competing against digital-first fintechs with AI-powered member experiences, megabanks with billion-dollar advertising budgets, and a generation of consumers who expect every financial interaction to happen seamlessly on their smartphones.

For credit union marketing leaders, the challenge isn’t just keeping pace—it’s fundamentally transforming how your institution acquires, engages, and retains members in an era where “digital branch” isn’t a metaphor; it’s your primary revenue driver.

This guide is designed for Chief Marketing Officers, VPs of Marketing and Directors of Member Growth who are tasked with lowering member acquisition costs, proving ROI to skeptical CFOs, and navigating the complex intersection of innovation and compliance. You’ll discover strategic frameworks, tactical playbooks, and the specific digital marketing approaches that are driving measurable growth in 2026.

1. The 2026 Credit Union Marketing Imperative

The GTM Transformation: Why Siloed Marketing Fails

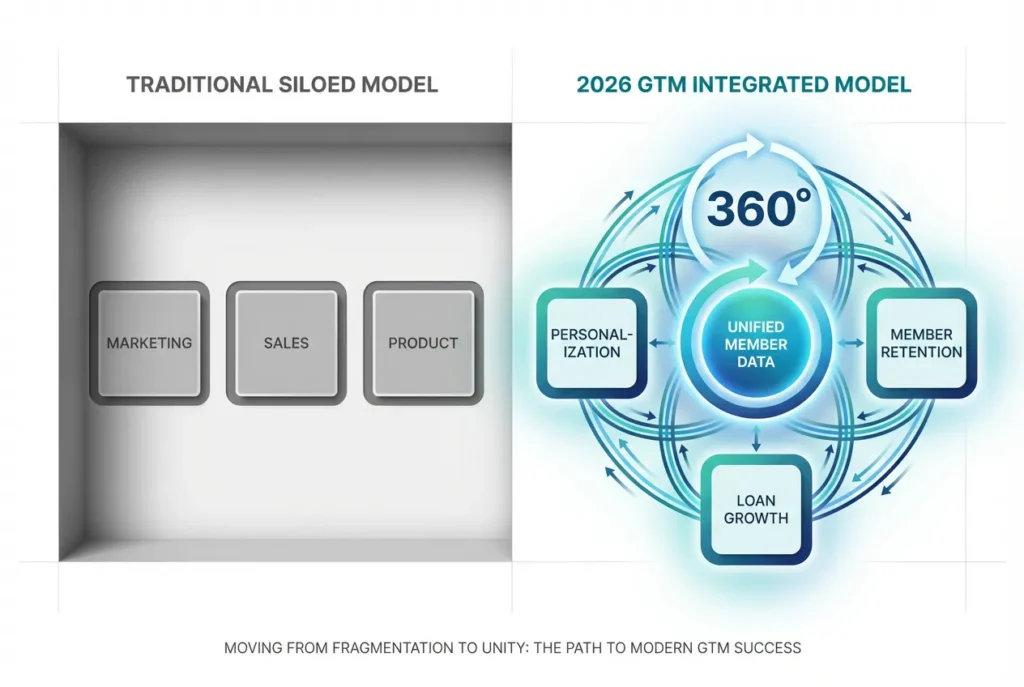

Credit unions have historically operated with distinct, independent departments—marketing promotes the brand, sales (member services) handles conversions, and product teams develop offerings in relative isolation. This fragmented approach worked when member journeys were linear and branch-centric.

In 2026, this model is breaking down.

The modern member journey is non-linear, omnichannel, and data-intensive. A prospective member might discover your credit union through a TikTok video about first-time home buying, research your auto loan rates via a ChatGPT query, compare your offerings on NerdWallet, and then expect to open an account entirely through their mobile device—all without ever speaking to a human.

The Go-To-Market (GTM) Transformation requires credit unions to integrate marketing, member services, and product development into a unified strategy with shared data, aligned KPIs, and seamless handoffs between digital touchpoints.

A comparison diagram showing the shift from siloed credit union departments to a 2026 GTM Integrated Model with unified member data and personalization.

Transitioning from siloed departments to an integrated Go-To-Market (GTM) strategy is essential for credit unions to compete with fintechs and achieve unified member data views in 2026.

Market Dynamics Reshaping Credit Union Growth

Industry Consolidation: The number of federally insured credit unions has declined by over 40% in the past two decades. Survivors are those that invest strategically in digital infrastructure and member experience.

The $10B Digital Sales Opportunity: According to industry research, digital channels now influence over 80% of loan originations, yet most credit unions have digital account opening abandonment rates exceeding 50%. Closing this gap represents the single largest growth opportunity available.

Winning Gen Z and Millennials: These demographics represent 73% of new account openings but expect mobile-first experiences, instant approvals, and personalized financial guidance. They’re not visiting branches—they’re researching on Reddit and comparing rates through AI assistants.

From Brand Awareness to Performance Acquisition

Traditional credit union marketing focused heavily on brand awareness: community sponsorships, billboards, radio ads emphasizing your “people helping people” philosophy. While brand equity matters, 2026 demands a fundamental shift toward performance acquisition marketing—strategies where every dollar spent can be traced to specific member actions, loan applications, and account openings.

This doesn’t mean abandoning brand building. It means your brand work must now integrate with measurable conversion pathways. Your community involvement generates content for social proof. Your sponsorships create retargeting audiences. Your thought leadership builds the E-E-A-T signals that help you rank in generative AI search results.

The credit unions winning in 2026 have marketing leaders who can present their CEO and CFO with clear member lifetime value (LTV) to customer acquisition cost (CAC) ratios—ideally 3:1 or higher—and demonstrate exactly how digital marketing investments translate into deposit growth and loan originations.

2. Search Everywhere & Generative Engine Optimization (GEO)

The Death of Traditional SEO (And What’s Replacing It)

For years, credit union marketers optimized websites to rank on Google’s search results pages. In 2026, that’s no longer enough.

The “Search Everywhere” Era means consumers are finding financial information through ChatGPT, Gemini, Perplexity, voice assistants, social media discovery feeds, and embedded AI within banking apps. A prospective member asking “What credit union has the best auto loan rates near me?” might never see a traditional Google search result—they’ll receive a conversational AI response synthesized from multiple sources.

Generative Engine Optimization (GEO) is the strategic approach to ensuring your credit union appears in these AI-generated responses. Unlike traditional SEO, which focuses on keywords and backlinks, GEO requires:

- Structured data markup that makes your rates, terms, and locations easily parsable by AI models

- Authoritative, detailed content that AI systems recognize as credible source material

- E-E-A-T signals (Experience, Expertise, Authoritativeness, Trustworthiness) that pass increasingly sophisticated quality filters

A mobile UI mockup illustrating Generative Engine Optimization (GEO) vs traditional search, highlighting E-E-A-T signal strength and AI responses.

As search evolves into Generative Engine Optimization (GEO), credit unions must prioritize E-E-A-T signals to ensure their loan products appear in AI-driven conversational search results.

Building E-E-A-T for Financial Services

Google and other AI systems evaluate financial content through a “Your Money or Your Life” (YMYL) framework—content that could impact financial well-being is held to the highest quality standards.

To pass these filters, your credit union must demonstrate:

Experience: Real member testimonials, case studies showing how families achieved financial goals through your institution, documented success stories with specific outcomes.

Expertise: Leadership profiles highlighting financial services credentials, CUNA certifications, years of industry experience. Bylined articles from your loan officers, CFP-certified advisors, and compliance officers.

Authoritativeness: Third-party recognition (awards, industry rankings, regulatory compliance records), media mentions, partnerships with recognized financial organizations.

Trustworthiness: Transparent rate disclosures, clear fee structures, accessible privacy policies, security certifications, positive online reviews across multiple platforms.

Tactical Implementation:

- Create individual bio pages for loan officers and member service leads with credentials, headshots, and expertise areas

- Publish detailed “Member Success Stories” featuring real names, photos (with permission), and specific financial outcomes

- Ensure every rate table includes disclosure details, APR calculations, and last-updated timestamps

- Secure backlinks from local news sites, chambers of commerce, and financial education platforms

Local SEO 2.0: Hyper-Local Branch Pages

Even as digital banking dominates, local presence remains a competitive advantage for credit unions. But ranking in local search requires far more sophistication than simply having a Google Business Profile.

Hyper-Local Branch Pages means creating unique, valuable content for each physical location:

- Community-specific financial content: “First-Time Homebuyer Programs in [Neighborhood],” “Small Business Lending for [City] Entrepreneurs”

- Local economic data: Employment statistics, median home prices, small business growth trends specific to that branch’s service area

- Branch-specific member testimonials: Stories from members who used that particular location

- Neighborhood involvement: Photos and descriptions of local events your branch sponsored or participated in

Google Business Profile “Community” Features: Google now allows businesses to create community posts, events, and Q&A responses directly within their profiles. Credit unions should use these to:

- Announce financial education workshops at specific branches

- Share local economic development news

- Answer common questions about membership eligibility, account opening requirements, and loan processes

- Promote branch-specific promotions (while ensuring NCUA compliance)

By creating this hyper-local content ecosystem, you signal relevance to both traditional search algorithms and AI models looking to provide location-specific financial guidance.

3. AI-Powered Member Acquisition & Hyper-Personalization

Beyond “Hi [First_Name]”: True 1:1 Personalization

Generic email marketing with first-name personalization is table stakes. In 2026, members expect experiences that feel individually crafted based on their financial situation, life stage, and goals.

Predictive Life Event Marketing uses transaction data and behavioral signals to identify when members are experiencing major life changes:

- New baby detected (baby store purchases, pediatrician payments) → Trigger content about 529 college savings plans and estate planning

- Home shopping indicated (realtor.com visits, mortgage calculator usage) → Deliver pre-qualification offers and first-time homebuyer education

- Career transition signals (LinkedIn profile updates, professional networking event charges) → Promote business banking services and commercial loan products

- Retirement approach (age + increased financial planning tool usage) → Offer wealth management consultations and distribution strategy guidance

This requires integrating your core banking system with marketing automation platforms and implementing AI models that can identify patterns without violating privacy expectations or regulatory requirements.

Implementing Ethical AI-Powered Personalization

The power of AI-driven personalization comes with significant compliance and ethical considerations:

Fair Lending Act Compliance: Your AI models must not create disparate impact on protected classes. Regular third-party audits of your algorithms ensure you’re not inadvertently discriminating based on race, gender, age, or other protected characteristics.

UDAAP Considerations: The CFPB scrutinizes marketing practices that could be Unfair, Deceptive, or Abusive. Your AI-generated content must be:

- Clear: APR calculations shown prominently, fees disclosed upfront

- Accurate: Real-time rate updates, no outdated promotional offers

- Non-deceptive: No implied guarantees that aren’t contractually supported

Privacy-First Data Usage: Members must have clear control over how their transaction data is used for marketing. Implement:

- Granular opt-in/opt-out controls within your digital banking platform

- Transparent explanations of what data drives which personalization

- Regular privacy impact assessments as your AI capabilities expand

Practical Implementation: The AI Marketing Stack for Credit Unions

To execute predictive, personalized marketing at scale, credit unions need integrated technology:

Core System Integration: Your Jack Henry Symitar, Fiserv DNA, or other core banking platform must feed transaction data into your marketing system (with appropriate member consent and data anonymization for aggregate analysis).

Marketing Automation Platform: Tools like HubSpot, Marketo, or specialized financial services platforms (Nymbus, Backbase) that can receive member data, segment audiences dynamically, and trigger personalized campaigns.

AI/ML Layer: Predictive models that identify life events, propensity to convert, and churn risk. This might be built in-house if you have data science capabilities, or through partnerships with vendors like Zafin, Ignite, or Salesforce Einstein for Financial Services.

Compliance Validation Engine: Real-time review of all AI-generated marketing content to ensure NCUA §740.5 compliance, Truth in Savings Act adherence, and state-specific advertising regulations. Some credit unions build rule-based systems; others use AI-powered compliance tools from vendors like Continuity, COMPLY, or Regtech platforms.

For many credit unions, building this stack in-house is neither practical nor cost-effective. Consider partnering with a B2B digital marketing agency that specializes in financial services and can provide both the technology integration and regulatory expertise required for sophisticated AI-driven campaigns.

4. The Digital Branch & Omnichannel Member Experience

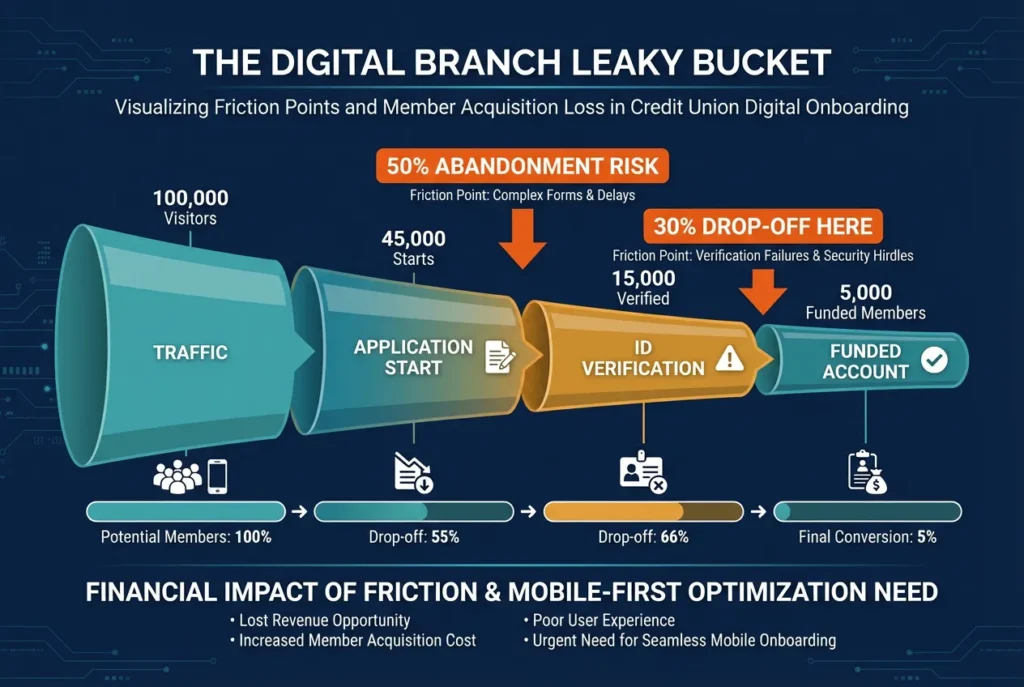

The 50% Problem: Digital Onboarding Abandonment

Your credit union likely invests significant marketing dollars driving traffic to your account opening pages. But industry data shows that over 50% of users who start a digital account application abandon before completion.

This “leaky bucket” represents your single largest conversion opportunity. Even modest improvements in digital onboarding conversion can dramatically increase member acquisition without any increase in marketing spend.

Common Abandonment Points:

- Identity verification failures (15-20% drop-off): Members can’t complete knowledge-based authentication or document upload processes feel cumbersome

- Funding friction (25-30% drop-off): Requirement to mail a check or visit a branch to make initial deposit

- Mobile optimization failures (10-15% drop-off): Forms don’t work properly on smartphones, too many fields require desktop completion

- Approval wait times (5-10% drop-off): No instant decision, members lose interest waiting 24-48 hours for manual review

A conversion funnel diagram for credit union digital onboarding, highlighting a 50% abandonment risk during the ID verification and funding stages.

Digital onboarding friction is the single largest barrier to member acquisition; identifying and fixing ‘leaky bucket’ stages can significantly improve the conversion of applications to funded accounts.

Solving the Digital Onboarding Challenge

Instant Identity Verification: Replace or supplement knowledge-based authentication (KBA) with document scanning (driver’s license photo upload with automated extraction), biometric verification, or real-time bank account verification through services like Plaid.

Remote Deposit Integration: Allow members to fund their first deposit via ACH transfer, debit card payment, or mobile check deposit—all within the application flow without leaving your website.

Progressive Onboarding: Don’t require every field upfront. Collect minimum information to open the account, then progressively gather additional data as the member uses your services. This reduces initial friction while maintaining compliance.

Mobile-First Form Design:

- Single-column layouts optimized for thumb navigation

- Auto-format phone numbers and social security numbers as users type

- Use device capabilities (camera for document scanning, GPS for address verification)

- Save progress automatically so members can return if interrupted

Instant Approval Engines: Work with your core provider or decision engine vendors (FICO, Experian, TransUnion) to implement automated approval rules for low-risk accounts. Many credit unions can safely approve 60-70% of applications instantly based on risk models.

The Hybrid Distribution Model: Physical + Digital

The future isn’t “digital only”—it’s strategically blended. Forward-thinking credit unions are implementing:

Micro-Branches (250-500 sq ft): Strategically placed in high-traffic retail locations, these aren’t traditional branches. They feature:

- 1-2 universal associates who can handle any member need

- Video banking for specialist consultations (mortgage officers, wealth advisors)

- Interactive digital displays for self-service transactions

- Appointment-driven model (book online, arrive for focused consultation)

Virtual Lobby Bankers: Members browsing your website or mobile app can instantly connect via video chat with a live banker for questions, applications, or problem resolution—during extended hours beyond traditional branch times.

Smart Branch Technology: Even full-service branches are becoming more efficient through:

- Interactive Teller Machines (ITMs) that provide extended hours with remote teller assistance

- Appointment scheduling systems that reduce wait times and match members with specialized staff

- Digital intake forms completed on tablets before meeting with loan officers

The goal is to provide members choice in how they interact with your credit union while ensuring each channel is optimized for efficiency and excellent experience.

5. Paid Media Strategy for $500M+ Asset Credit Unions

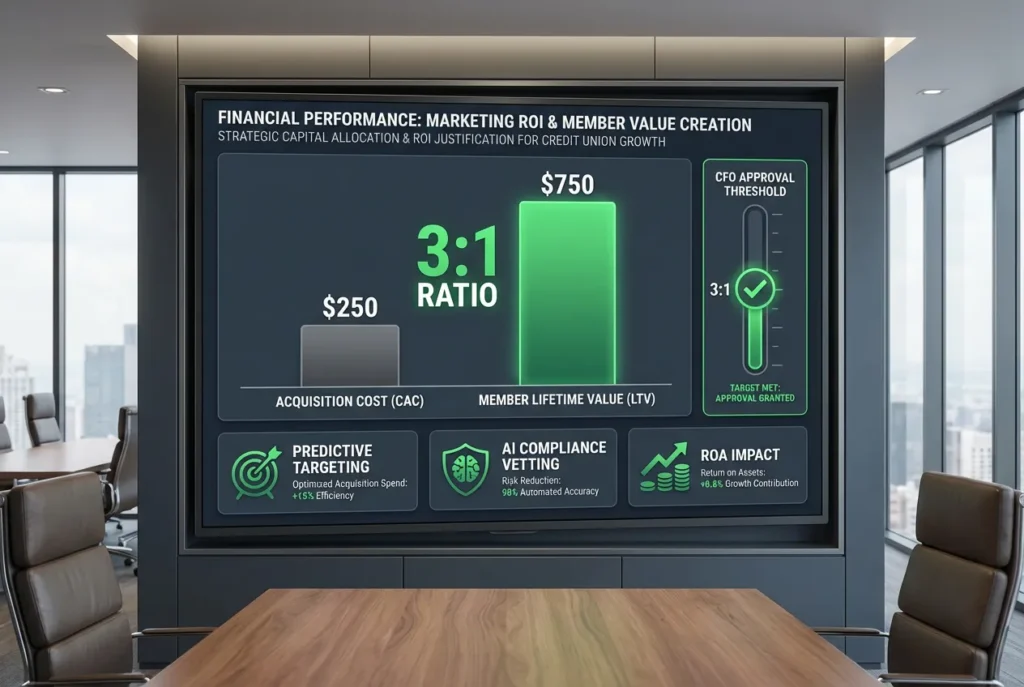

The CFO Perspective: Proving the 3:1 LTV:CAC Ratio

Before diving into channel tactics, understand this reality: Your CEO and CFO care about one metric above all others—Member Lifetime Value (LTV) to Customer Acquisition Cost (CAC) ratio.

For credit unions, a healthy ratio is 3:1 or higher. That means the total net revenue you’ll generate from a member over their relationship (deposits, loan interest, fee income) should be at least 3x what it cost to acquire them.

Calculating Member LTV:

Average member relationship length (years) × Average annual net revenue per member (interest income on loans + net interest income on deposits + fee income – cost to serve)

Calculating Customer Acquisition Cost:

Total marketing spend (paid media, content, personnel, agency fees, technology) ÷ Number of new members acquired

Many credit union marketers struggle to secure budget because they can’t demonstrate this fundamental relationship. Investing in attribution tracking, member cohort analysis, and financial modeling is essential before requesting significant paid media budgets.

A financial bar chart demonstrating a 3:1 Member Lifetime Value to Acquisition Cost ratio, designed for credit union CFO and executive presentations.

Securing marketing budget for 2026 requires proving a 3:1 LTV:CAC ratio; this financial model demonstrates how predictive targeting and AI efficiency drive sustainable credit union growth.

Channel Strategy: Where to Invest Your Paid Media Budget

Google Search (25-35% of paid budget):

Your highest-intent channel. Members actively searching “best auto loan rates [city]” or “credit union near me” are ready to compare and convert.

- Loan-specific campaigns: Separate campaigns for auto, mortgage, personal, HELOC, and business loans with dedicated landing pages

- Location-based bidding: Higher bids for searches near your branches, lower bids for areas outside your field of membership

- Competitor conquesting: Bid on competitor credit union and bank names (check NCUA guidance on comparative advertising)

- Shopping ads for loan products: If permitted by Google (emerging capability), showcase your rates directly in search results

Facebook & Instagram (20-30% of budget):

Your awareness and consideration channel. Perfect for storytelling, member testimonials, and financial education that builds affinity before purchase intent.

- Interest-based targeting: Target users interested in home buying, new cars, small business ownership, retirement planning

- Life event targeting: Facebook allows targeting of newly engaged, recently moved, new parents—all high-value audiences for credit unions

- Lookalike audiences: Upload your best member lists (high deposit balances, multiple products), Facebook creates similar audience segments

- Video content: Short-form educational videos dramatically outperform static image ads

LinkedIn (15-25% of budget, B2B-focused credit unions):

If you serve commercial members and businesses, LinkedIn is essential for reaching decision-makers.

- Treasury services campaigns: Target CFOs, controllers, finance managers at local businesses

- Commercial loan products: Reach small business owners, entrepreneurs, franchisees

- Wealth management services: Target high-income professionals, executives, physicians for advisory relationships

- Thought leadership content: Promote financial education content to build expertise positioning

Facebook Groups (Organic + Sponsored):

Building moderated communities creates incredible brand affinity and positions your credit union as the trusted financial partner.

- First-Time Homebuyer Groups: Provide education, Q&A, connect with mortgage officers

- Local Business Owner Communities: Networking + financial tips for commercial members

- Financial Wellness Groups: General personal finance education demonstrating your commitment to member success

Display/Programmatic (10-15% of budget):

For brand awareness and retargeting users who visited your site but didn’t convert.

- Retargeting campaigns: Show product-specific ads to users who viewed loan pages but didn’t apply

- Geofencing: Serve ads to devices detected at competing bank branches, car dealerships, real estate open houses

- Contextual targeting: Display ads on financial news sites, mortgage comparison sites, auto research platforms

Measurement Beyond Clicks: Attribution Models for Credit Unions

Traditional “last-click attribution” dramatically undervalues awareness channels. A member might discover your credit union through Instagram, research rates on your website, compare you against competitors, and then finally convert via a Google search for your name.

Last-click attribution gives all credit to that final Google branded search—ignoring the Instagram ad that started the journey.

Implement Multi-Touch Attribution:

- First-touch model: Gives credit to the channel that introduced the member

- Linear model: Distributes credit equally across all touchpoints

- Time-decay model: Gives increasing credit to touchpoints closer to conversion

- Data-driven model: Uses machine learning to assign credit based on actual conversion patterns in your data

Most credit unions need outside expertise to implement sophisticated attribution. Consider working with a specialized financial services marketing agency that understands both the technical implementation and the unique compliance requirements of credit union marketing attribution.

6. Compliance, Security, and Governance in Digital Marketing

NCUA Advertising Rule §740.5: 2026 Updates

The NCUA’s advertising regulations exist to ensure credit unions don’t mislead potential members. Recent guidance clarifications affect digital marketing significantly:

Required Disclosures:

- Membership eligibility: You must clearly state who can join (geographic area, employer group, association membership)

- Rate accuracy: APRs must be current (many credit unions now use dynamic rate feeds from core systems to website)

- Fee disclosures: Material fees that affect the true cost must be disclosed

- Share insurance: “Federally insured by NCUA” must appear on marketing materials

Digital-Specific Considerations:

- Social media: Brief form disclosures acceptable if clear link to full terms available

- Video ads: Disclosures must be visible long enough to read (typically 5+ seconds)

- Email marketing: Disclosures in email body preferred over requiring click to external page

- Mobile ads: Space constraints acknowledged but key disclosures still required

What You CAN Simplify in 2026:

Recent NCUA guidance allows removing some technical disclaimers from advertising materials if they’re clearly available in account agreements. This applies primarily to standard fee schedules and terms—not to rate disclosures or material product limitations.

Work with your compliance officer to determine exactly which disclosures are mandatory in paid ads versus account opening materials. Many credit unions are too conservative, creating cluttered ads that underperform.

ADA Digital Access: The 2026 Lawsuit Wave

Website accessibility lawsuits targeting financial institutions have increased 300% since 2020. Credit unions are prime targets because many have under-invested in WCAG (Web Content Accessibility Guidelines) compliance.

High-Risk Areas:

- PDF rate sheets: If not tagged for screen readers, these are frequent lawsuit triggers

- Online banking login: Must be fully keyboard-navigable without mouse

- Account opening forms: Error messages must be screen-reader compatible

- Video content: Captions required for all member-facing videos

Compliance Framework:

Follow WCAG 2.1 Level AA standards as minimum:

- All images have descriptive alt text

- Color contrast ratios meet minimums (4.5:1 for normal text)

- All functionality available via keyboard only

- Form fields have proper labels associated

- Dynamic content updates announced to screen readers

Don’t just run automated accessibility checkers—hire actual disabled users or specialized firms to conduct manual testing. Automated tools catch only about 25-30% of accessibility issues.

Third-Party Vendor Liability:

Your credit union is responsible for accessibility of ALL digital properties—including those provided by vendors. Your online banking provider, loan application system, and mortgage calculators must all be accessible. Include WCAG 2.1 AA compliance as a contractual requirement with all technology vendors.

Data Privacy in the Age of Personalization

Hyper-personalized marketing requires significant member data. Balancing personalization with privacy is both an ethical and legal imperative.

State-Level Privacy Regulations:

California (CCPA/CPRA), Virginia (VCDPA), Colorado (CPA), Connecticut (CTDPA), and Utah (UCPA) have comprehensive consumer privacy laws affecting how credit unions can collect and use member data. Key requirements:

- Opt-out rights: Members must be able to opt out of data sale/sharing (define “sharing” broadly to include marketing pixels)

- Purpose limitation: Only use data for purposes disclosed at collection

- Deletion rights: Members can request deletion of their data (with reasonable exceptions for regulatory record-keeping)

Marketing Technology Privacy:

Every marketing pixel, tracking code, and analytics tool on your website potentially “shares” member data with third parties:

- Google Analytics: Transmits IP addresses, behavior data to Google

- Facebook Pixel: Shares page views, conversions with Meta

- Hotjar/FullStory: Records session replays including form interactions

Conduct a thorough audit of all tracking technologies. Update your privacy policy to accurately describe all data sharing. Implement consent management platforms (OneTrust, Osano, Termly) that allow members granular control.

Security Considerations for Digital Campaigns

Phishing Prevention: Your marketing emails must be clearly identifiable as legitimate to prevent member victimization:

- Implement DMARC/SPF/DKIM email authentication

- Use recognizable, consistent sender names and email addresses

- Never include links to login pages in promotional emails (direct to public site only)

- Include language like “We will never ask for your password via email”

Landing Page Security: All account opening and loan application pages must use HTTPS with current TLS certificates. Display trust badges from Norton, McAfee, or BBB accreditation prominently.

Ad Fraud Protection: Financial services are prime targets for click fraud and bot traffic that can quickly exhaust paid media budgets without generating real member applications. Implement:

- IP address filtering to block known bot networks

- Click pattern analysis to identify fraudulent activity

- Geographic restrictions aligned with your field of membership

- Partner with platforms like ClickCease, PPC Protect, or Fraud Blocker

For credit unions without in-house security expertise, working with an agency that specializes in government and regulated industries marketing ensures both performance and protection against fraud.

Frequently Asked Questions

Q: How much should credit unions with $500M+ in assets budget for digital marketing in 2026?

A: Industry benchmarks suggest 0.5-1.5% of total assets for comprehensive marketing (including personnel, technology, and media spend). For a $500M credit union, that’s $2.5M-$7.5M total.

Digital should represent 60-70% of that budget ($1.5M-$5.25M), with approximately 40% going to paid media, 30% to technology and automation, 20% to content and creative, and 10% to analytics and optimization. The key is demonstrating ROI through clear LTV:CAC ratios and incremental member acquisition—if you can prove a 3:1 or better return, you can justify increased investment.

Q: What’s the single most important digital marketing capability for credit unions to develop in 2026?

A: Unified member data. Without the ability to see a complete view of each member across core banking, digital banking, website behavior, email engagement, and paid media touchpoints, you cannot execute personalized campaigns, measure true attribution, or optimize member lifetime value.

This requires breaking down system silos and implementing a Customer Data Platform (CDP) or data warehouse that integrates all sources. This foundation enables everything else—AI personalization, accurate attribution, lifecycle marketing—making it the highest-leverage investment.

Q: How do we handle digital marketing for credit unions with field of membership restrictions?

A: Geotargeting and audience exclusion are your tools. In paid media platforms: Set radius-based targeting around eligible areas. For employment-based membership (e.g., “employees of X company”), use LinkedIn’s employer targeting or Facebook’s employer interest targeting.

Create gated content requiring membership eligibility verification before accessing rate information for highly restricted products. Use website personalization to show different calls-to-action based on visitor location (eligible visitors see “Open Account,” non-eligible see “Learn About Membership”).

Most importantly, clearly state eligibility requirements in all advertising to avoid generating unqualified applications—this actually improves CAC by focusing spend on convertible audiences.

Q: Can credit unions use member testimonials and success stories in digital advertising while maintaining privacy?

A: Yes, but you need explicit written consent. The NCUA requires that any use of member endorsements or testimonials be truthful and not misleading, and privacy regulations require clear consent for using personal information in marketing.

Best practice: Create a testimonial consent form that specifically authorizes use of name, photo, and story in digital marketing channels. Compensate members fairly (gift cards, fee waivers, charitable donations in their name) and ensure the compensation is disclosed in the advertisement.

For added protection, consider using “composite members”—fictional representations based on real member patterns but not identifiable individuals—for some storytelling.

Q: What’s the most effective content marketing strategy for credit unions trying to compete with fintechs?

A: Financial education content that solves real problems without requiring an immediate product sale. Fintechs excel at product UX but often lack deep financial guidance.

Credit unions can win by creating comprehensive resources: “Complete Guide to Building Business Credit,” “First-Time Homebuyer Financial Timeline,” “Small Business Cash Flow Management Playbook.” Make this content genuinely valuable, ungated (to maximize SEO reach), and demonstrate expertise through data, case studies, and clear explanations.

Position your loan officers and financial advisors as the authors to build E-E-A-T. This content serves both SEO (attracting early-stage researchers) and sales enablement (your member service staff can share specific articles). The key is consistency—publish weekly, comprehensively optimize for search, and promote through email and social.

Q: Should credit unions build internal digital marketing teams or partner with agencies?

A: For most $500M+ credit unions, the optimal model is a hybrid: small strategic internal team (2-4 people including a senior marketing leader) partnered with specialized agency or fractional CMO services.

The internal team provides industry knowledge, compliance oversight, and stakeholder management. The agency provides specialized expertise (paid media optimization, conversion rate optimization, technical SEO, AI implementation) that’s inefficient to hire in-house.

This model provides flexibility to scale efforts up/down based on performance without the fixed cost and turnover risk of large internal teams. The exception: credit unions over $2B in assets may justify bringing more capabilities in-house, but even then, specialized functions like account-based marketing for commercial lending often benefit from agency expertise.

Q: How do we measure the impact of brand awareness campaigns versus direct response in credit union marketing?

A: Implement brand lift studies and multi-touch attribution simultaneously. For brand awareness efforts (social media content, display advertising, community sponsorships), conduct regular brand lift surveys measuring aided and unaided awareness, consideration, and preference in your field of membership.

Compare these metrics against control groups that haven’t been exposed to your campaigns. For direct response (Google Search, retargeting, conversion-focused campaigns), use last-click conversion tracking as your minimum benchmark but implement multi-touch attribution to understand the full journey.

The key insight: brand awareness campaigns create the environment where direct response succeeds. Members who’ve been exposed to your awareness campaigns convert at higher rates and lower costs when they later search for loan products. Run incrementality tests where you turn off awareness campaigns in specific geographies and measure the impact on direct response performance to quantify this relationship.

Q: What compliance considerations are most important for credit unions using AI in digital marketing?

A: Three critical areas: fair lending, privacy, and explainability. For fair lending compliance, your AI models must not create disparate impact on protected classes.

This requires regular adverse impact analysis—measuring whether different demographic groups receive significantly different marketing treatments or approval rates. Document that any differences are based on legitimate, non-discriminatory business factors. For privacy compliance, ensure your AI personalization clearly discloses what member data is being used and provides meaningful opt-out mechanisms that don’t disadvantage members who exercise privacy rights.

For explainability, you must be able to explain to regulators how your AI models make decisions. Pure “black box” neural networks are high-risk; use models where you can document decision logic. Work with legal counsel to document AI governance frameworks that demonstrate appropriate oversight and regular bias audits.

Taking Action: Your 2026 Digital Marketing Roadmap

Digital transformation for credit unions isn’t a single project—it’s an ongoing evolution. Based on the strategies outlined in this guide, here’s how to prioritize your next steps:

Immediate Actions (30 days):

- Audit your digital onboarding conversion funnel to identify the biggest abandonment points

- Review all paid media landing pages for NCUA §740.5 compliance and WCAG accessibility

- Implement proper multi-touch attribution tracking if not already in place

- Calculate your current member LTV:CAC ratio for each acquisition channel

Short-Term Priorities (90 days):

- Develop comprehensive buyer personas based on member data analysis, not assumptions

- Optimize your Google Business Profiles for all branches with community-specific content

- Begin structured data markup implementation for loan products to enable GEO readiness

- Launch pilot campaigns on your two highest-potential paid media channels with rigorous A/B testing

Medium-Term Initiatives (6-12 months):

- Implement marketing automation integrated with your core banking system for personalized lifecycle campaigns

- Develop comprehensive content libraries addressing each stage of the member journey for key product categories

- Rebuild your website with mobile-first, conversion-optimized architecture

- Establish formal governance frameworks for AI use in marketing including compliance reviews and bias testing

Long-Term Transformation (12-24 months):

- Complete GTM transformation integrating marketing, sales, and product teams around unified member data

- Achieve full omnichannel capability where members can seamlessly switch between digital and physical channels

- Develop predictive AI models for propensity to purchase, churn risk, and lifetime value scoring

- Build a measurement ecosystem that can clearly attribute member acquisition across all touchpoints and prove ROI to executive leadership

The credit unions that thrive in 2026 and beyond will be those that view digital marketing not as a tactical advertising function, but as a strategic growth engine integrated across the entire member experience. This requires investment, expertise, and often external partnership to execute at the level required to compete effectively.

If your credit union is ready to accelerate this transformation, Chatter Buzz specializes in financial services digital marketing with deep expertise in compliance-first campaign execution, sophisticated member acquisition strategies, and the data integration required to prove ROI.

Our team understands the unique challenges of credit union marketing—from field of membership restrictions to regulatory oversight—and has helped institutions like yours achieve measurable growth through strategic digital transformation.

The member acquisition landscape has fundamentally changed. The question isn’t whether to invest in sophisticated digital marketing—it’s whether your credit union will lead or follow in this new era.