Multicultural Credit Union Marketing: Reach Every Community

The U.S. population is more diverse than at any point in history — and credit unions that still market as if their entire field of membership looks the same are leaving millions in deposits and loan originations on the table.

Multicultural marketing for credit unions isn’t a DEI checkbox. It’s a growth strategy. We’ve seen credit unions that invested in culturally relevant campaigns for Hispanic, Black, Asian American, and immigrant communities grow membership 2-3x faster in those segments than their general market campaigns. The math is clear.

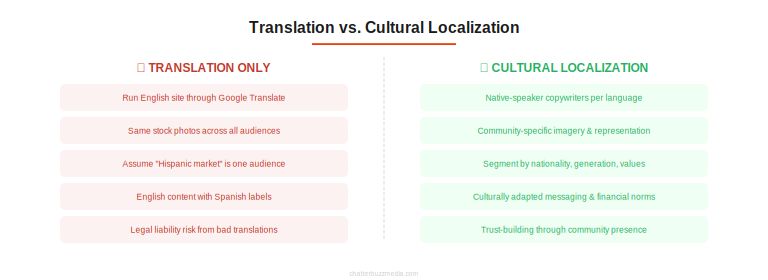

This guide walks you through how to build a multicultural marketing strategy that goes beyond translation — because running your English website through Google Translate and calling it “outreach” isn’t a strategy. It’s a liability.

Key Takeaways

- Multicultural marketing is a growth strategy, not a compliance exercise. Hispanic, Black, and Asian American communities represent the fastest-growing segments of the U.S. population — and they’re actively looking for financial institutions that understand their needs.

- Translation is not localization. Running English content through Google Translate creates legal risk and destroys trust. Culturally adapted messaging that reflects community values, financial norms, and communication preferences is the standard.

- Community presence beats digital reach in multicultural markets. Sponsoring cultural festivals, partnering with community organizations, and hiring from within the community builds trust that no ad campaign can replicate.

- Financial literacy content in native languages is the highest-trust entry point. First-time homebuyer workshops in Spanish, retirement planning seminars for Vietnamese communities, and small business guides for Haitian entrepreneurs create real relationships.

- Representation matters at every level — your staff, your board, your imagery, and your branch locations should reflect the communities you serve. Members notice.

- Measure by community segment, not aggregate. Track membership growth, deposit growth, and loan origination by demographic segment to identify what’s working and where to invest more.

The Undeniable Imperative: Why Multicultural Marketing is Non-Negotiable for Credit Unions

The Demographic Tsunami Reshaping Financial Services

The numbers tell a story that credit union leaders can no longer ignore:

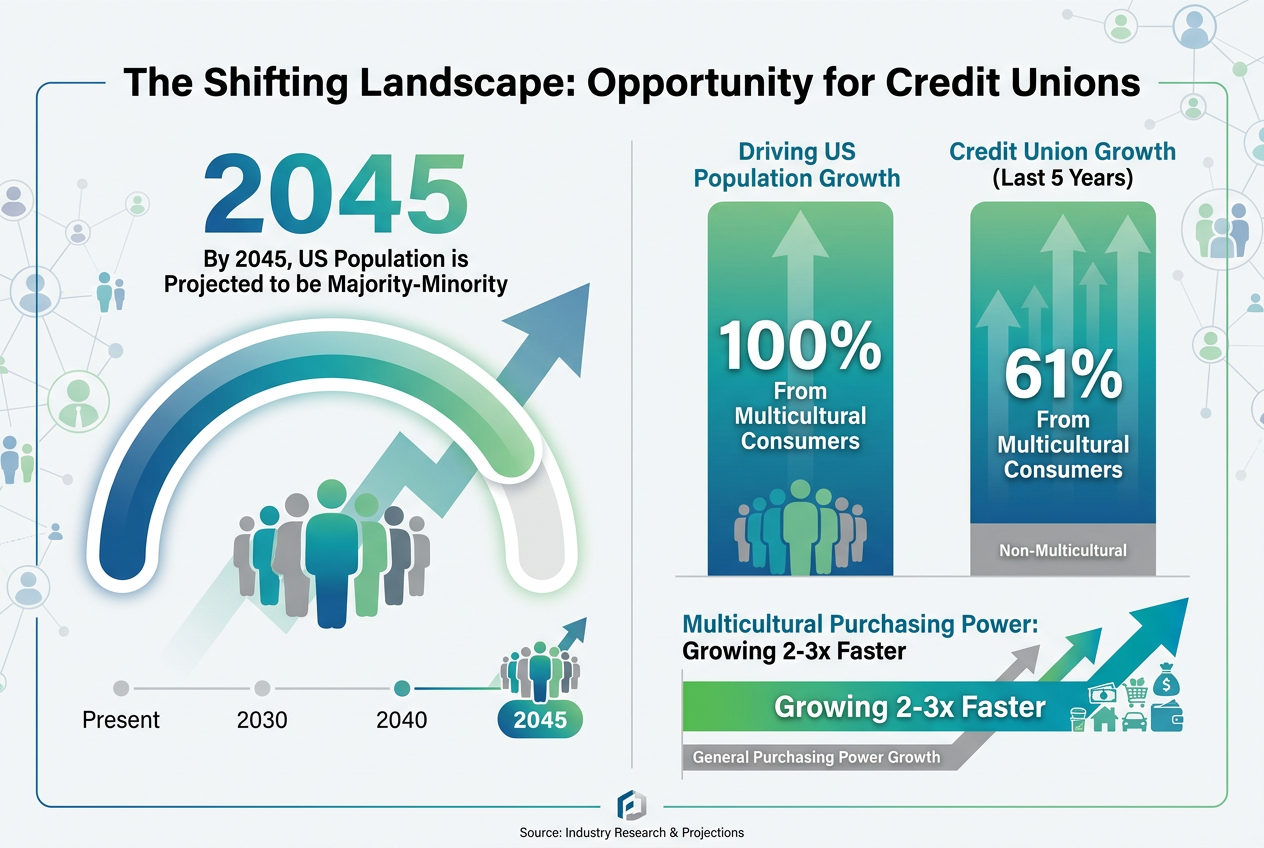

- By 2045, the U.S. will be a majority-minority nation, with multicultural populations representing the majority of Americans

- Multicultural consumers are driving 100% of population growth in the United States, while the non-Hispanic white population is declining

- 61% of credit union growth over the last five years came from multicultural members

- Young, multicultural consumers represent the future: millennials and Gen Z are significantly more diverse than previous generations

These aren’t projections for some distant future—these demographic shifts are happening right now, transforming your field of membership whether you’re prepared or not.

Economic Power Creating Unprecedented Opportunity

Beyond sheer population growth, multicultural communities represent explosive economic power:

- Hispanic purchasing power is growing 2-3 times faster than non-Hispanic white consumers, exceeding $2.8 trillion annually

- Asian American buying power has increased by over 257% since 2000, reaching $1.3 trillion

- Black consumer spending surpasses $1.6 trillion annually, with higher propensity for certain financial products like payment protection and life insurance

For credit unions competing for deposits and loan volume, these communities represent not just growth opportunity but survival. The question isn’t whether you can afford to invest in multicultural marketing—it’s whether you can afford not to.

The Unbanked and Underbanked: Your Blue Ocean Opportunity

Approximately 7.1 million U.S. households remain unbanked, with disproportionately high rates among Hispanic (12.2%), Black (13.8%), and other minority households. Another 18.7 million households are underbanked, relying on alternative financial services.

This represents both a tremendous business opportunity and a chance to fulfill your credit union’s cooperative mission by providing fair, accessible financial services to communities historically exploited by predatory lenders.

Competitive Imperatives: Adapt or Become Irrelevant

While you’re considering multicultural marketing strategies, your competitors are already executing them:

- Fintechs are designing mobile-first experiences specifically for younger, diverse consumers who expect seamless digital banking

- Megabanks are investing millions in Spanish-language advertising, bilingual branches, and culturally relevant products

- Challenger banks are targeting specific ethnic communities with tailored offerings and culturally competent service

The cost of inaction is existential: credit unions that fail to adapt will watch their membership age, their competitive position erode, and their community relevance diminish until they’re forced into mergers or closure.

This visual highlights the critical demographic shifts and economic power of multicultural consumers, underscoring why an inclusive marketing strategy is essential for credit union growth and relevance.

Beyond Translation: Understanding the Nuances of Diverse Communities

Defining “Multicultural” in Credit Union Context

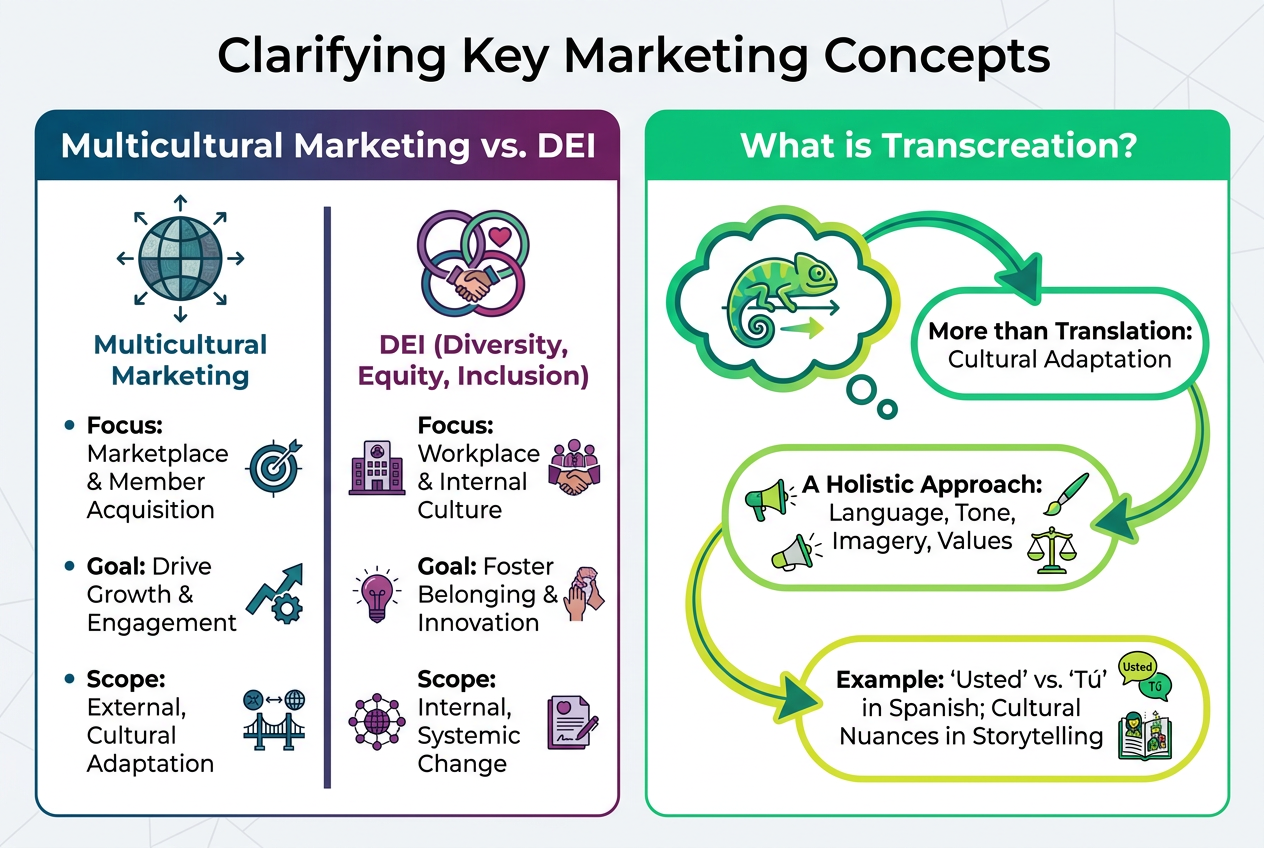

First, let’s clarify what we mean by multicultural marketing. While diversity encompasses race, ethnicity, age, gender, sexual orientation, ability, socioeconomic status, religion, and geography, we’re focusing specifically on marketplace strategies—how you market to and serve diverse member segments.

This differs from diversity, equity, and inclusion (DEI) initiatives, which primarily address your internal workforce and culture. However, as we’ll explore, the two are deeply interconnected: you cannot market authentically to diverse communities without first cultivating an inclusive internal culture.

Hispanic Communities: A Deeper Dive into Your Fastest-Growing Segment

When credit unions think about multicultural marketing, Hispanic consumers often represent the largest immediate opportunity. However, “Hispanic” isn’t a monolith—it encompasses tremendous diversity:

Country of Origin Matters: A Mexican-American member in Texas may have completely different financial behaviors and cultural values than a Puerto Rican member in Florida or a Cuban-American in Miami.

Generational Differences Are Significant: First-generation immigrants often prefer Spanish-language services and have different trust levels with financial institutions than second or third-generation Hispanic Americans who may be fully bilingual or English-dominant.

Cultural Values Shape Financial Decisions: Family (familia) is paramount in Hispanic culture, influencing everything from who makes financial decisions to saving priorities. Community and personal relationships often matter more than interest rates when choosing a financial institution.

Specific Financial Needs and Behaviors: Hispanic consumers are more likely to:

– Send remittances to family in their home countries

– Prefer cash and alternative payment methods

– Lack traditional credit histories but demonstrate creditworthiness through alternative data

– Value financial education and guidance, especially for first-time homebuyers

Understanding these nuances is crucial for developing products, services, and marketing messages that genuinely resonate rather than tokenize.

The Power of “Transcreation”: Beyond Word-for-Word Translation

Here’s where most credit unions fail: they believe that translating their English website into Spanish constitutes multicultural marketing. It doesn’t.

Transcreation means adapting your message culturally, not just linguistically. It requires understanding:

Cultural References and Imagery: Stock photos of white nuclear families don’t resonate with Hispanic audiences. Your visuals should authentically reflect the communities you’re trying to serve—multigenerational households, extended families, community gatherings.

Tone and Formality: Should you use “usted” (formal you) or “tú” (informal you) in Spanish communications? The answer depends on your brand positioning and target demographic. Formal language builds respect; informal language builds connection.

Cultural Values and Attitudes: CUNA Mutual Group discovered that their beneficiary designation forms confused many Hispanic members because Latino culture views death and life insurance fundamentally differently than Anglo culture. Understanding these values isn’t just good marketing—it’s essential for product design.

Storytelling Approaches: Individualistic achievement narratives that work in mainstream American marketing may fall flat with cultures that prioritize collective success and family obligation.

Effective transcreation requires native speakers who understand both the language and the culture—ideally members of the community you’re serving.

Addressing Unconscious Biases That Undermine Your Efforts

Even well-intentioned credit unions often make assumptions that reveal unconscious bias and ultimately alienate the communities they’re trying to serve:

The “One-Size-Fits-All” Trap: Assuming all Hispanic members speak Spanish, or that all Black members share the same financial behaviors, demonstrates a lack of cultural competence that members notice.

The “Curb Cut Effect”: PixelSpoke’s research highlights a powerful concept: designing for outliers benefits everyone. When you create products and processes that serve diverse needs—like offering forms in multiple languages or accepting alternative credit data—you often improve the experience for all members.

Deficit-Based Thinking: Viewing multicultural communities through a lens of what they lack (credit history, documentation, English proficiency) rather than what they bring (strong community ties, entrepreneurial drive, loyalty to institutions that serve them well) sabotages authentic relationship-building.

Overcoming these biases requires more than diversity training—it demands ongoing commitment to listening to diverse voices within your organization and your membership.

Understand the crucial differences between multicultural marketing and DEI, and grasp the power of ‘transcreation’ to connect authentically by adapting content culturally, not just linguistically.

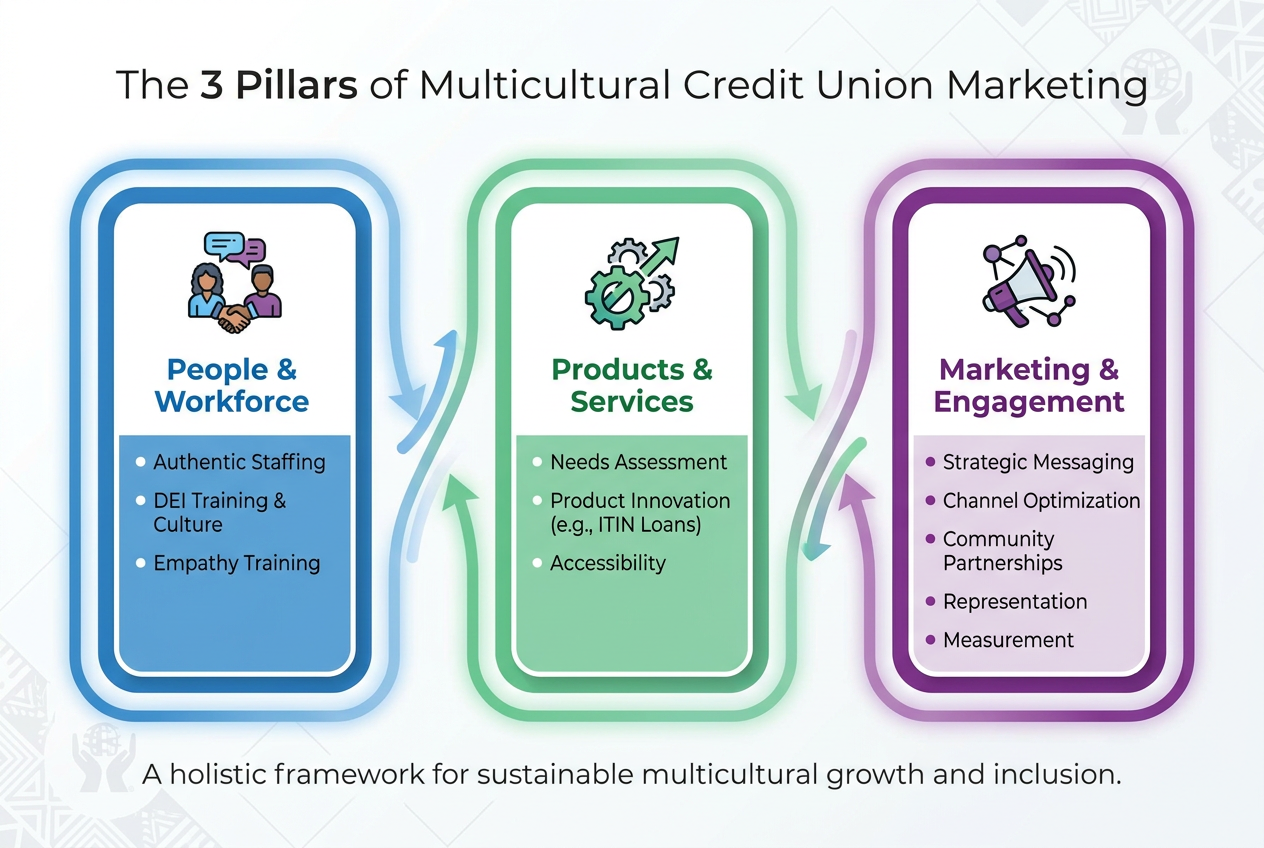

Building Your Multicultural Marketing Strategy: A 3-Pillar Framework

Successfully reaching Hispanic and diverse communities requires a holistic approach that extends far beyond marketing communications. Our three-pillar framework—People & Workforce, Products & Services, and Marketing & Engagement—provides a comprehensive roadmap for credit unions at any stage of their multicultural journey.

This framework provides a strategic roadmap for credit unions, integrating internal readiness, product innovation, and authentic engagement to build a successful multicultural marketing strategy.

Pillar 1: People & Workforce (Internal Foundation)

Your multicultural marketing strategy will fail if it’s not supported by an authentically inclusive internal culture. This pillar focuses on the people delivering your member experience.

Authentic Staffing: Beyond Automated Translation

The brutal truth: Automated translation tools and generic call center scripts cannot replace genuine cultural competence and linguistic fluency.

Successful multicultural credit unions prioritize:

Bilingual/Bicultural Staff in Key Touchpoints: Hire staff who are native speakers and cultural natives in your target communities—not just employees who took Spanish in high school. Position them in:

– Branch locations serving diverse communities

– Call centers and member service

– Lending departments where complex financial decisions require nuanced communication

– Leadership positions where they can influence strategy

Cultural Competence Training: Implement ongoing training that goes beyond compliance to build genuine understanding of diverse member needs, communication styles, and cultural values.

Compensation and Career Development: Pay competitive rates for bilingual skills and create clear pathways for advancement. Too many credit unions exploit bilingual employees by paying them the same as monolingual staff while expecting them to serve two member populations.

Building an Inclusive Workplace Culture

Before you can authentically market to diverse communities, you must create an internal environment where diverse employees thrive:

DEI as Foundation: While distinct from multicultural marketing, your diversity and inclusion initiatives directly impact your ability to serve diverse members. Credit unions with homogeneous leadership and staff lack the perspectives needed for genuine cultural competence.

Employee Resource Groups: Create affinity groups for Hispanic, Black, Asian, LGBTQ+, and other employees to share experiences, provide cultural insights, and advise on initiatives.

Inclusive Decision-Making: Ensure diverse voices are represented when making decisions about products, policies, and marketing strategies that affect multicultural communities.

Cultivating Empathy and Cultural Humility

Empathy Training: Teach staff to recognize their own cultural assumptions and develop genuine curiosity about members’ experiences and needs.

Community Immersion: Encourage employees to participate in community events, learn about cultural traditions, and build relationships beyond transactional member interactions.

Mistake Recovery: Create a culture where staff can acknowledge cultural missteps, learn from them, and improve—rather than one where fear of getting it wrong prevents authentic engagement.

Pillar 2: Products & Services (Meeting Specific Needs)

Multicultural marketing isn’t just about how you promote existing products—it’s about developing offerings that address the specific financial needs of diverse communities.

Conducting Meaningful Needs Assessment

Data-Driven Understanding: Analyze your existing member data by demographic segments to identify:

– Product utilization patterns

– Loan approval rates and reasons for denial

– Digital banking adoption

– Member satisfaction scores

– Attrition rates

Community Research: Don’t just rely on internal data. Conduct focus groups, surveys, and interviews with members and non-members from diverse communities to understand:

– Financial challenges and goals

– Banking preferences and behaviors

– Barriers to accessing financial services

– Unmet needs and desired products

Psychographic and Behavioral Insights: Go beyond demographics to understand values, attitudes, and behaviors that influence financial decisions within different cultural contexts.

Product Innovation That Drives Inclusion

Based on needs assessment, consider developing or adapting products such as:

ITIN Loans: Individual Taxpayer Identification Number (ITIN) loans serve immigrants without Social Security numbers, opening credit access to a significantly underserved market. Several credit unions have built thriving portfolios serving this segment.

International Money Transfer Services: With billions sent in remittances annually, offering competitive international transfer services with transparent fees addresses a critical need for many Hispanic members while generating fee income.

Alternative Credit Scoring: Partner with fintech providers that use alternative data (rent payments, utility bills, cell phone payments) to evaluate creditworthiness beyond traditional credit scores, expanding access to members with thin credit files.

Small-Dollar Loans: Develop responsible small-dollar loan products that compete with predatory payday lenders while helping members build credit and avoid destructive debt cycles.

Credit-Building Programs: Offer secured credit cards, credit-builder loans, and financial coaching to help members establish or rebuild credit.

Culturally Relevant Insurance Products: Partner with providers offering insurance products that address specific cultural needs, such as burial insurance or policies that cover family members abroad.

Business Banking for Immigrant Entrepreneurs: Many immigrant communities have high rates of entrepreneurship. Develop business banking products, microloans, and support services tailored to immigrant-owned businesses.

Ensuring Accessibility Across All Channels

Bilingual Digital Platforms: Offer fully translated (and transcreated) websites, mobile apps, and online banking in relevant languages, with the ability to seamlessly switch languages.

Multichannel Access: Recognize that different generations and cultural groups have varying preferences for in-person, phone, and digital banking. Maintain strong branch presence while investing in digital.

Financial Literacy Programs: Develop educational content and workshops in multiple languages, addressing topics particularly relevant to immigrant and diverse communities (building credit, homebuying, small business financing, retirement planning).

Pillar 3: Marketing & Engagement (Reaching and Connecting)

With your internal foundation and product suite in place, you’re ready to execute marketing strategies that authentically reach and engage diverse communities.

Strategic Messaging That Resonates

Address Specific Pain Points: Your messaging should speak directly to the financial challenges diverse communities face:

– “Build your credit history without a Social Security number”

– “Send money home safely and affordably”

– “Achieve homeownership in your new country”

Lead with Values, Not Just Rates: While competitive rates matter, multicultural consumers often prioritize trust, personal relationships, and values alignment. Emphasize:

– Your cooperative structure and member-ownership

– Community investment and support

– Cultural competence and welcoming environment

– Long-term financial partnership, not transactional banking

Authentic Representation: Feature real members from diverse communities in testimonials and case studies. Avoid stock photos that feel inauthentic or tokenistic.

Culturally Relevant Storytelling: Use narrative approaches that resonate culturally—family success stories, community impact, multi-generational achievement.

Channel Optimization for Diverse Audiences

Social Media Strategy: Different demographic and cultural segments favor different platforms:

– Facebook: Still dominant among older Hispanic and immigrant populations

– Instagram: Popular with younger, bilingual Hispanic consumers

– WhatsApp: Essential for staying connected with many immigrant communities

– TikTok: Growing influence among young diverse audiences

– LinkedIn: Effective for reaching professionals and business owners

Spanish-Language Media: Invest in:

– Spanish-language radio (still highly influential in many Hispanic markets)

– Spanish-language television and streaming platforms

– Hispanic-focused newspapers and online publications

– Bilingual community publications

Digital-First Approach: Younger multicultural consumers expect sophisticated digital experiences. Prioritize:

– Mobile-optimized everything (mobile is often the primary or only internet access)

– Video content with captions and translations

– Interactive tools and calculators

– Seamless digital account opening

Search Engine Optimization: Optimize your website for Spanish-language searches and multilingual queries. Many bilingual consumers code-switch between languages when searching.

For more guidance on driving member growth through digital channels, explore our guide to B2B demand generation.

Community Engagement and Partnerships

Sponsorship and Events: Support community organizations, cultural festivals, and events that serve diverse populations. Show up consistently, not just during Hispanic Heritage Month or Black History Month.

Partnership with Community Organizations: Build relationships with:

– Immigrant resource centers

– Hispanic chambers of commerce

– Faith-based organizations serving diverse communities

– Cultural centers and mutual aid societies

– ESL programs and adult education centers

Financial Literacy Initiatives: Offer workshops and resources on topics critical to diverse communities:

– Understanding the U.S. financial system

– Building credit from scratch

– First-time homebuyer education

– Small business financing

– Avoiding financial fraud targeting immigrant communities

Employee Advocacy: Empower your bilingual/bicultural staff to be ambassadors in their communities, attending events, serving on nonprofit boards, and building trust through personal relationships.

Measuring and Optimizing Performance

Track Specific KPIs by Demographic Segment:

– New member acquisition from target communities

– Product penetration rates (loans, credit cards, digital banking)

– Member satisfaction scores

– Referral rates

– Cross-sell ratios

– Share of wallet

– Member lifetime value

Digital Marketing Metrics:

– Website traffic and engagement from Spanish-language pages

– Social media engagement rates by language and demographic

– Cost per acquisition (CPA) for multicultural campaigns

– Conversion rates through multilingual landing pages

Attribution and ROI: Use marketing analytics tools and CRM data to understand which channels and tactics drive the strongest return on investment for different segments. Learn more about marketing automation strategies to streamline your tracking.

Continuous Improvement: Multicultural marketing is not a one-time initiative but an ongoing commitment to learning, adapting, and deepening relationships with diverse communities.

Overcoming Challenges & Driving ROI

Addressing Internal Resistance and Securing Leadership Buy-In

Even with compelling demographic data, you may encounter internal resistance to multicultural marketing initiatives. Here’s how to overcome common objections:

The “We Don’t Want to Alienate Our Current Members” Concern

The Reality: Inclusive marketing doesn’t alienate existing members—in fact, research shows that diverse representation in marketing makes brands more appealing across all demographics. The “curb cut effect” applies to marketing: making your credit union more welcoming to diverse communities improves the experience for everyone.

The Response: Frame multicultural marketing as expanding your reach, not replacing current strategies. You’ll continue serving existing members while growing your relevance with new demographics.

The “We Don’t Have the Budget” Objection

The Reality: You can’t afford not to invest. The cost of inaction—declining membership, shrinking deposits, diminished community relevance—far exceeds the investment in multicultural marketing.

The Response: Present the business case with data:

– Growth potential in diverse segments

– Declining demographics in traditional member base

– Competitive threats from institutions already serving these markets

– Lower customer acquisition costs through community partnerships

– Higher member lifetime value in underserved markets

Start with pilot programs in high-opportunity markets to demonstrate ROI before scaling broadly.

The “Our Staff Isn’t Equipped” Reality

The Solution: This is a legitimate concern that requires investment in:

– Bilingual hiring (which may require adjusting compensation structures)

– Cultural competence training

– Translation and transcreation services

– Partnerships with multicultural marketing agencies like a specialized performance marketing agency that specialize in financial services

View this as capacity-building, not just cost. The capabilities you develop serve your organization long-term.

Demonstrating Clear ROI and Business Impact

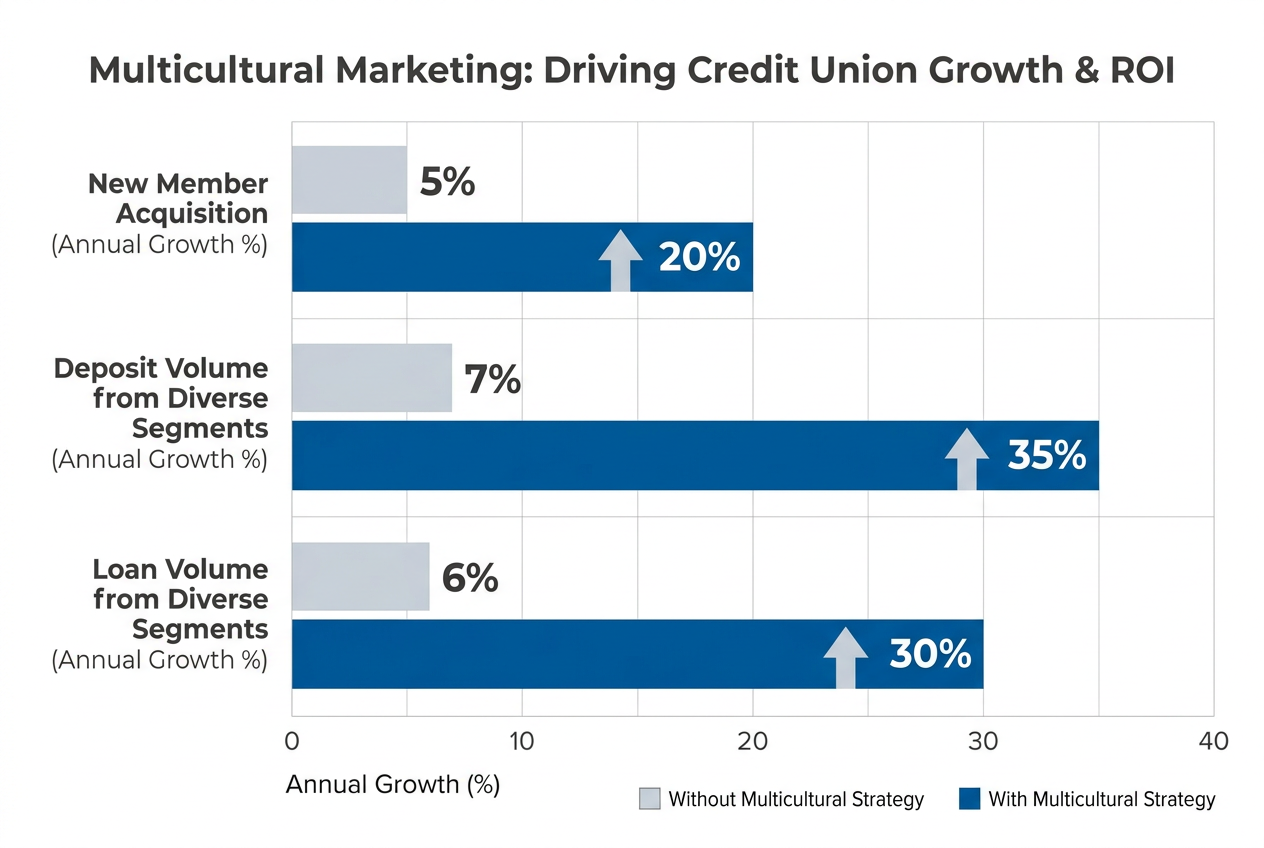

Visualize the clear business case for investing in multicultural marketing, showing how it dramatically increases new member acquisition, deposit growth, and loan volume from diverse communities.

To secure ongoing investment and support, connect multicultural marketing directly to the KPIs your leadership cares about:

New Member Acquisition: Track new members from target demographic segments, with cost per acquisition compared to traditional marketing channels. Typically, community-based multicultural marketing yields lower CPAs and higher lifetime values.

Deposit Growth: Measure deposit volume from diverse member segments. Many immigrant communities have high savings rates but are underbanked—capturing these deposits strengthens your institution’s financial position.

Loan Volume: Track loan originations to diverse members, including products specifically designed for underserved segments (ITIN loans, alternative credit programs). Calculate portfolio performance and risk.

Digital Banking Adoption: Measure enrollment and usage of mobile banking, online banking, and other digital services among diverse members. Younger multicultural members often drive digital adoption.

Member Satisfaction and Retention: Survey diverse members specifically to gauge satisfaction and identify improvement opportunities. Calculate retention rates and attrition compared to overall membership.

Share of Wallet: Measure how many products diverse members hold compared to other segments. Cross-sell opportunities often increase as trust deepens.

Market Share Growth: Track your credit union’s growth in serving diverse communities compared to competitors in your market.

The Cost of Inaction vs. The Value of Investment

Let’s be clear about what’s at stake:

If you don’t invest in multicultural marketing:

– Your membership will continue aging as younger, diverse consumers choose competitors

– Your deposit base will erode as diverse communities grow wealth outside your institution

– Your community relevance will diminish as demographics shift

– Your competitive position will weaken against institutions already serving these markets

– You’ll face pressure to merge or be acquired as growth stagnates

If you do invest strategically in multicultural marketing:

– You’ll position your credit union for sustainable growth in the communities driving population expansion

– You’ll fulfill your cooperative mission by serving historically underserved populations

– You’ll develop competitive advantages through deep community relationships

– You’ll build a more inclusive organizational culture that attracts top talent

– You’ll future-proof your institution against demographic change

The choice isn’t whether multicultural marketing is worth the investment—it’s whether your credit union has a future.

Frequently Asked Questions

1. 🌍 What is the difference between multicultural marketing and diversity and inclusion (DEI)?

Multicultural marketing focuses on marketplace strategies—how you reach, engage, and serve diverse customer or member segments through tailored products, services, and marketing communications. DEI initiatives primarily address your internal workforce culture, hiring practices, and organizational inclusion. However, the two are interconnected: you cannot market authentically to diverse communities without first building an inclusive internal culture with diverse perspectives informing your strategy.

2. 💬 How do I start a multicultural marketing strategy for my credit union if I have a limited budget?

Start with research and pilots in high-opportunity areas. Begin by analyzing your existing member data to identify diverse segments and their specific behaviors and needs. Conduct focus groups or surveys with members and non-members from target communities. Pilot initiatives in one geographic area or with one product category, measure results rigorously, and use that ROI data to justify expanded investment. Partner with community organizations for low-cost ways to build trust and awareness. Even translating key website pages and hiring one bilingual branch staff member is a meaningful start that demonstrates commitment.

3. 📊 What’s the biggest mistake credit unions make with Hispanic marketing?

The biggest mistake is treating translation as strategy. Simply translating English marketing materials into Spanish word-for-word misses cultural nuances, values, and context that determine whether messaging resonates. Effective Hispanic marketing requires “transcreation”—cultural adaptation that considers imagery, tone, cultural values, and communication preferences. Additionally, many credit unions use one generic approach for all Hispanic consumers, ignoring significant differences based on country of origin, generation, language preference, and acculturation level. Finally, relying on automated translation tools or non-native speakers to create Spanish content often results in awkward, inauthentic messaging that undermines trust.

4. 🏦 How long does it take to see ROI from multicultural marketing initiatives?

Multicultural marketing is a long-term relationship-building strategy, not a quick-win tactic. Community-based approaches typically take 6-12 months to show measurable results as you build trust, awareness, and relationships. However, certain tactics can produce faster results: targeted digital advertising to specific demographic segments can generate leads within weeks, and partnering with established community organizations can accelerate credibility. The key is measuring both short-term indicators (website traffic, event attendance, lead generation) and long-term outcomes (member acquisition, product penetration, deposit growth) while maintaining consistent presence and commitment even before immediate ROI is visible.

5. 🤝 Do I need to hire bilingual staff or can I use translation services?

You absolutely need bilingual/bicultural staff in member-facing roles—translation services and technology cannot replace genuine cultural competence and fluent communication. Automated translation tools make grammatical errors and miss cultural context. More importantly, diverse members want to interact with staff who understand their lived experiences, not just their language. That said, professional translation and transcreation services are valuable for marketing materials, website content, and written communications. The ideal approach combines bilingual staff for personal interactions with professional translation services for content creation, all guided by native speakers who understand both language and culture.

6. 💰 How do I measure the success of my multicultural marketing efforts?

Track both demographic-specific metrics and overall business impact. Key performance indicators include: new member acquisition from target communities (with cost per acquisition compared to other channels), deposit and loan volume from diverse segments, product penetration rates, digital banking adoption, member satisfaction scores, retention and attrition rates, referral rates, and market share growth in target demographics. On the marketing side, measure website traffic and engagement from multilingual pages, social media engagement by language and demographic, conversion rates through culturally tailored campaigns, and campaign ROI. Use CRM data and marketing analytics tools to attribute results to specific initiatives and continuously optimize based on what drives the strongest return.

7. 🌍 Should I create separate marketing campaigns for different ethnic groups or one inclusive campaign?

The answer is both. You need an overarching brand message that emphasizes inclusion and welcomes all, but you also need targeted campaigns that speak specifically to different cultural segments with tailored messaging, imagery, language, and channels. A young, English-dominant second-generation Hispanic professional has different needs and preferences than a recent Spanish-speaking immigrant. An Asian-American entrepreneur seeking business banking requires different messaging than a Black millennial looking for a first mortgage. Successful multicultural strategies balance inclusive brand positioning with segment-specific campaigns that demonstrate deep understanding of particular communities. Start with the segments representing your biggest opportunities, execute those well, then expand to additional communities.

8. 💬 What are the compliance considerations for multicultural marketing in financial services?

Financial institutions must ensure all marketing materials, regardless of language, comply with NCUA, CFPB, FTC, and other regulatory requirements. This includes accurate disclosures, clear terms and conditions, fair lending compliance, and truth in advertising across all languages. Importantly, your Spanish or other language versions must convey the same information, disclosures, and legal terms as English versions—not simplified or abbreviated content. Work with compliance officers and legal counsel when developing multilingual materials. Additionally, ensure your bilingual staff understand compliance requirements and can explain products, terms, and conditions accurately in multiple languages. Document your multicultural marketing policies and train staff on fair lending and equal credit opportunity principles to avoid discriminatory practices.

Conclusion: Growth Lives in the Communities You Haven’t Reached Yet

The credit unions dominating membership growth in 2026 aren’t the biggest — they’re the ones that made specific communities feel seen, understood, and served. Every multicultural market you invest in today becomes a compounding growth engine as word-of-mouth spreads within tight-knit communities.

Start here:

- Identify your top 2-3 underserved communities — look at your field of membership demographics vs. your actual membership demographics. The gap is your opportunity.

- Hire or partner from within — bring in staff, advisors, or community liaisons who are already trusted in those communities. No amount of marketing replaces authentic representation.

- Create one high-value resource in each language — a first-time homebuyer guide in Spanish, a small business banking guide in Haitian Creole, a digital banking tutorial in Vietnamese. Start with what matters most to each community.

- Show up in person — sponsor a cultural festival, host a financial literacy workshop at a community center, partner with a local church or temple. Digital reach follows physical trust.

The communities you invest in today will become your most loyal, most vocal, and most valuable members for decades.

Next step: Download our complete guide to digital marketing for credit unions or explore our credit union marketing services.

Victoria Wallace

Victoria Wallace is a senior content strategist and marketing writer with 30+ years of experience helping more than 200 brands translate complex business goals into clear, conversion-focused content. Her background spans paid media, marketing strategy, go-to-market planning, brand positioning, and full-funnel campaign development, giving her a deep understanding of how SEO content connects to real business growth.